Spot major IUL policy red flags. Learn to evaluate misleading IUL illustrations, hidden fees, and cap rates with help from Life Policy Express.

Indexed Universal Life (IUL) insurance is becoming more popular. Many people choose it for lifelong coverage and the opportunity to grow cash value with the market. But these policies can be confusing, and sometimes they are sold with too much hype or not enough explanation.

Some IUL policies look good on paper but have hidden fees or use unrealistic projections. If you know what to watch out for, you can avoid buying a policy that lets you down later. This guide will show you the main warning signs and help you spot an IUL policy that is not right for you.

Indexed Universal Life (IUL) insurance is a form of permanent life insurance that combines a death benefit with a cash value account. The interest credited to the cash value is tied to the performance of an external equity index, like the S&P 500, but is subject to contractual caps and floors.

Your cash value is not actually invested in the stock market. The insurance company uses special strategies to follow the index. Most policies have a floor, often 0%, so you do not lose money if the market drops.

The catch is that there is a limit on how much you can earn. This is called a cap or participation rate. For example, if the index goes up 15% but your cap is 9%, you only get 9% credited to your cash value.

The primary red flags of a bad IUL policy include an IUL illustration that misleads you by showing maximum historical interest rates, rising internal Cost of Insurance (COI) charges that drain cash value over time, low cap rates below industry averages, and steep surrender charges lasting over a decade.

When you look at an insurance plan, it helps to have an independent expert check the details. Here are some warning signs to watch for:

Every permanent life policy comes with a sales illustration. Be careful if the agent only shows you the best possible returns from the past rather than a more realistic average.

If the presentation relies on a constant, aggressive annual return of 7% or 8% across forty straight years, the calculation ignores real-world volatility and market correction cycles. Under current NAIC consumer protection standards, carriers must follow strict benchmark limits on illustrated returns. If an illustration appears to focus solely on extreme wealth accumulation while ignoring basic contract safeguards, it is a bad sign for an IUL policy.

With an IUL, your premium is split. Some pay for fees, some for the insurance itself, and the rest goes into your cash value.

The cost of insurance goes up as you get older. If your policy is underfunded, these costs can eat up your cash value. If that happens, you might have to pay a lot more just to keep your coverage.

How much your cash value can grow depends on the cap and participation rates set by the insurance company. According to NerdWallet, the cap is the maximum rate you can earn during a specific period, while the participation rate determines the portion of the index gain that applies to your account. Caps can change while your policy is in force, so if an insurer lowers the cap from a competitive level, such as 10 percent, to a lower floor, such as 3 or 4 percent, your potential for accumulation could be significantly reduced.

Most permanent insurance contracts feature a surrender fee schedule designed to protect the carrier from the costs of early policy cancellations. However, if your contract restricts your access to funds and imposes high surrender penalties lasting 12 to 15 years, the plan lacks liquidity. This is a clear indicator that the coverage design is poorly aligned with dynamic lifestyle changes or emergency cash needs.

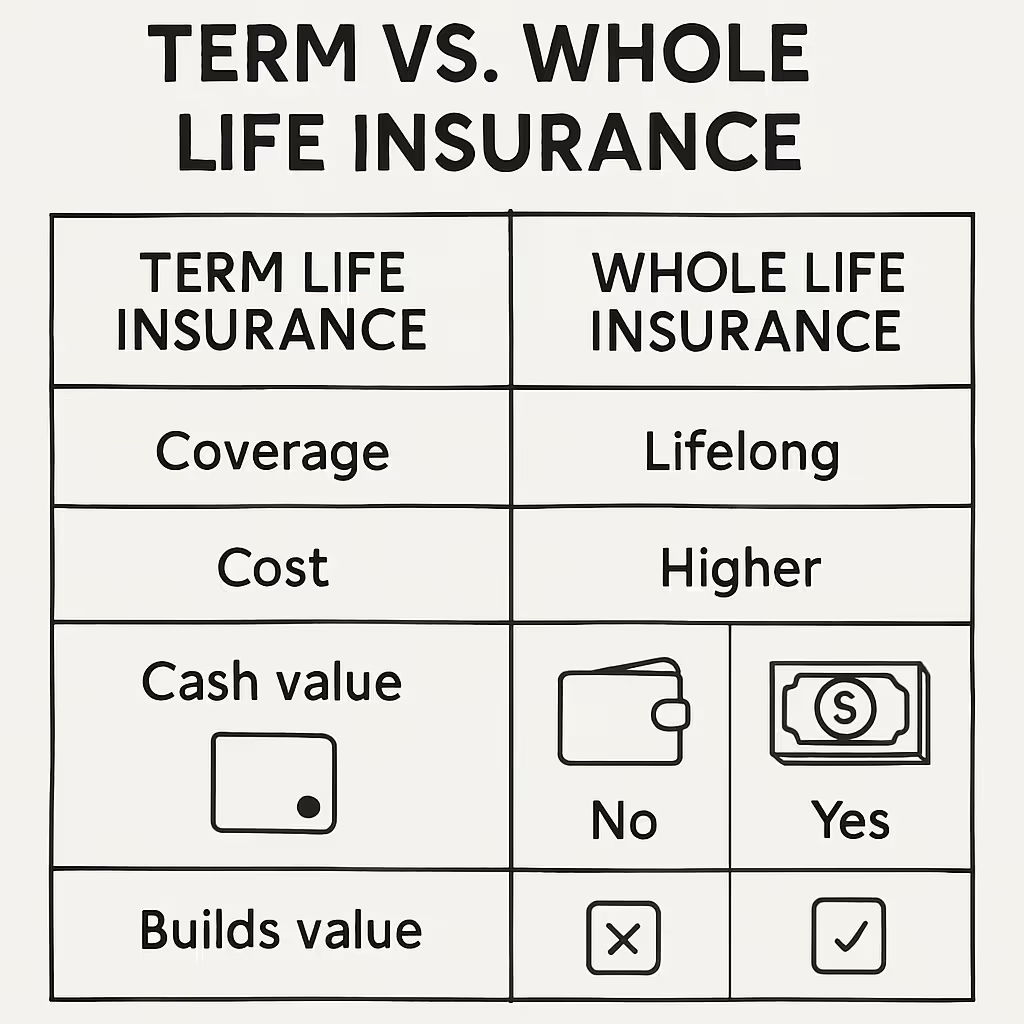

Neither product is universally superior; choice depends on your specific risk profile. Whole life insurance offers contractually guaranteed premiums, death benefits, and cash growth. Indexed universal life offers adjustable premiums and flexible death benefits, trading guarantees for market-linked accumulation potential.

To better understand these options, look at how the core structures compare side by side:

Choosing a path that avoids IUL policy risks involves weighing certainty against flexibility. Here is a simple comparison of how these two types of policies work: safer or final expense protection. On the other hand, an appropriately structured IUL policy offers premium flexibility for business owners or mass-affluent buyers looking for alternative, tax-advantaged accumulation tools.

To avoid IUL problems, you need clear information and advice from a real expert. According to Forbes Advisor, many large online platforms and call centers use automated processes to prioritize selling a high volume of insurance policies, which may not always ensure that the coverage fits your individual needs. Life Policy Express takes a different approach. We make insurance simple and personal by connecting you with a local advisor who works with you one-on-one.