Are you wondering what happens if you stop paying life insurance premiums? Learn how to manage the life insurance lapse grace period, avoid losing your coverage, and discover your options for recovery.

Life is unpredictable. Rising costs, job changes, or unexpected bills can force you to make tough choices about which household expenses to focus on. If you are experiencing financial difficulty, you might be wondering what happens if you stop paying life insurance premiums.

Stopping your payments can put years of sound financial planning at risk, leaving your loved ones without the safety net they rely on. However, a single missed payment does not mean instant disaster. Understanding the life insurance lapse grace period is your first step in crisis management. If you fail to act in time, you risk a complete life insurance lapse, which can have permanent financial consequences.

This guide presents supporting data and advanced strategies to accompany our comprehensive pillar post, “The Complete Guide to Life Insurance: Everything You Need to Know.” Below, we will explore the timeline of a missed payment, alternatives to canceling, and the exact steps required to recover your coverage.

A grace period is a contractually defined window of time after a missed payment during which your life insurance policy remains fully active. If your premium is due on the first of the month and your payment fails, your coverage does not vanish on the second day.

Instead, the life insurance lapse grace period begins immediately. Here is what you need to know about this critical window:

If the deadline passes without a payment being made, you face a life insurance lapse. This is the formal termination of your insurance contract due to non-payment. From this moment on, you are no longer covered, and the insurer is not legally obligated to pay a claim.

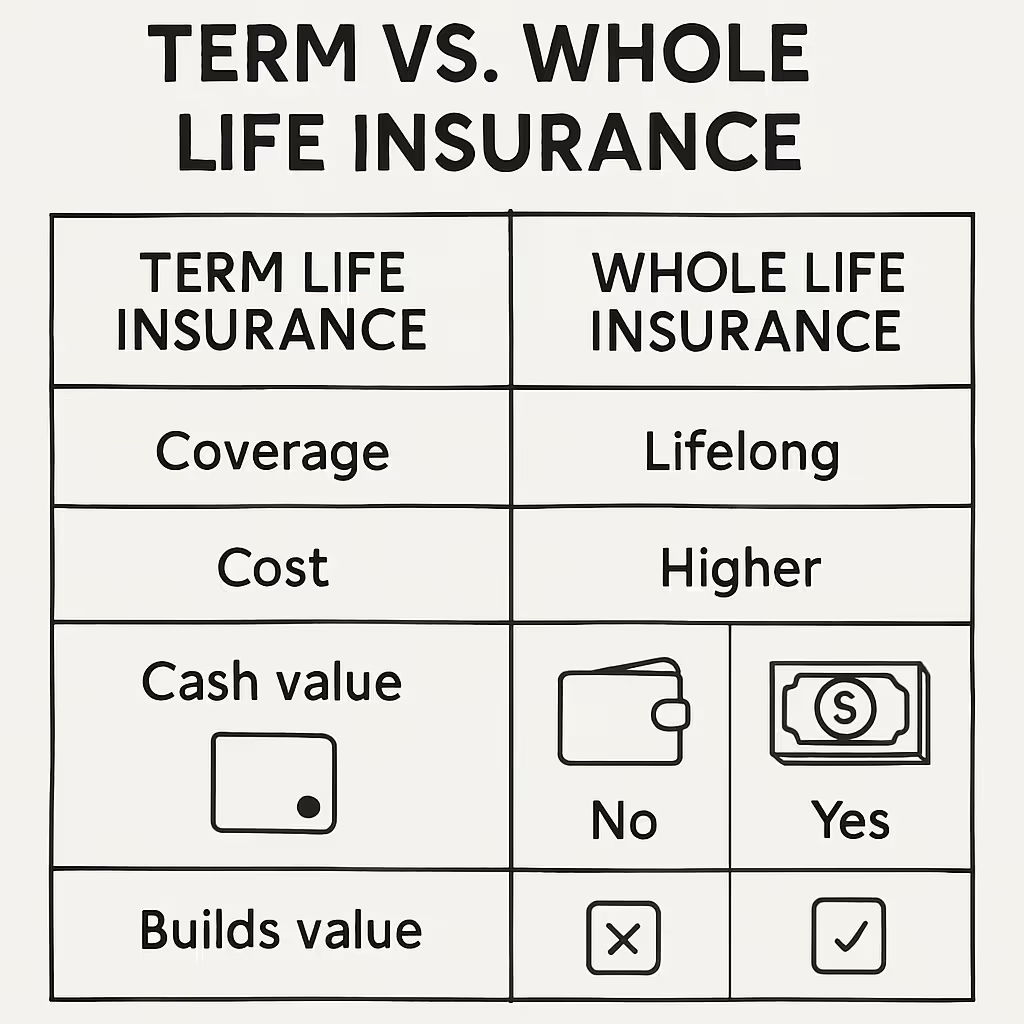

How this impacts you depends entirely on the type of life insurance you own:

If you are facing financial hardship, letting your policy expire is not your only option. Before walking away from your life insurance policy, consider these planned alternatives:

If your coverage has already officially terminated, most insurers provide a way to reactivate it. Pursuing a policy reinstatement is almost always a smarter financial move than starting over from scratch. The reinstatement process generally allows you to restore your coverage within a two to five-year window after the cancellation date.

To successfully complete a policy reinstatement, you must:

Why is reinstating life insurance policy coverage usually the better choice? First, it locks in the premium rates based on your original age and health status from when you initially bought the policy. Applying for a brand-new life insurance policy is generally much more expensive because you are older, and any new health conditions could result in a denial of coverage.

Furthermore, buying a new policy restarts the “contestability period.” This is a standard 1- to 2-year window during which insurers have the right to investigate and potentially deny a death claim due to inaccuracies in the application. Reinstating life insurance policy benefits usually lets you avoid reopening this risky window.

A prominent point to remember is that insurance companies have strict legal obligations. They are required to send clear, unmistakable notices before terminating your coverage for non-payment.

If the insurer fails to send these notices to the correct address, ignores a third-party designee, or sends unclear communications, the cancellation might be legally invalid. Families have successfully fought insurers in court to overturn a cancellation and secure their rightful death benefit when proper notification protocols were ignored.

Finding the right coverage during a financial transition can be incredibly stressful for buyers. That is why having a well-equipped, modern insurance advisor makes all the difference. Our platform, https://lifepolicyexpress.com/, is designed to help insurance agents improve their game and deliver superior, proactive service to you.

Here is how our platform empowers agents to protect buyers:

Using these modern tools, agents transform from simple salespeople into strategic advisors, making sure you always have the most accurate life insurance guidance when it matters most.

A missed premium payment is a critical warning sign, but it does not have to be the end of your financial security net. By knowing the timeline of the life insurance lapse grace period, you have the power to take strategic action and protect your family’s future.

Whether you are negotiating a temporary payment holiday, adjusting your coverage amounts, or actively reinstating life insurance policy benefits, there are numerous pathways to recovery. To prevent future stress, consider setting up automatic payments linked to a primary bank account or switching to annual billing to save 3% to 5% on processing fees. If you are ever facing a financial difficulty, do not wait in silence: contact your agent or insurer immediately before your window of opportunity closes.