Learn how to build a high-performance insurance agent compensation structure. Master 2026 commission trends, bonus tiers, and regulatory compliance tips.

To build a strong team in 2026, you need to balance rewarding your agents’ expertise with keeping your agency profitable. Independent agents have more choices than ever, so it’s important to offer a clear pay structure and reward real performance. Agencies that do this attract and keep the best agents. Start with a fair commission plan: offer high first-year commissions and steady renewals. Effective agent compensation is the foundation for attracting and retaining top talent.

If you want your agents to perform at their best, add tiered bonuses based on key numbers like how many policies stay active and how much business your agents write. Make sure your incentives encourage agents to prioritize long-term client relationships. When you build your pay plan around transparency, compliance, and putting clients first, you equip your team to offer honest, helpful advice that sets your agency apart.

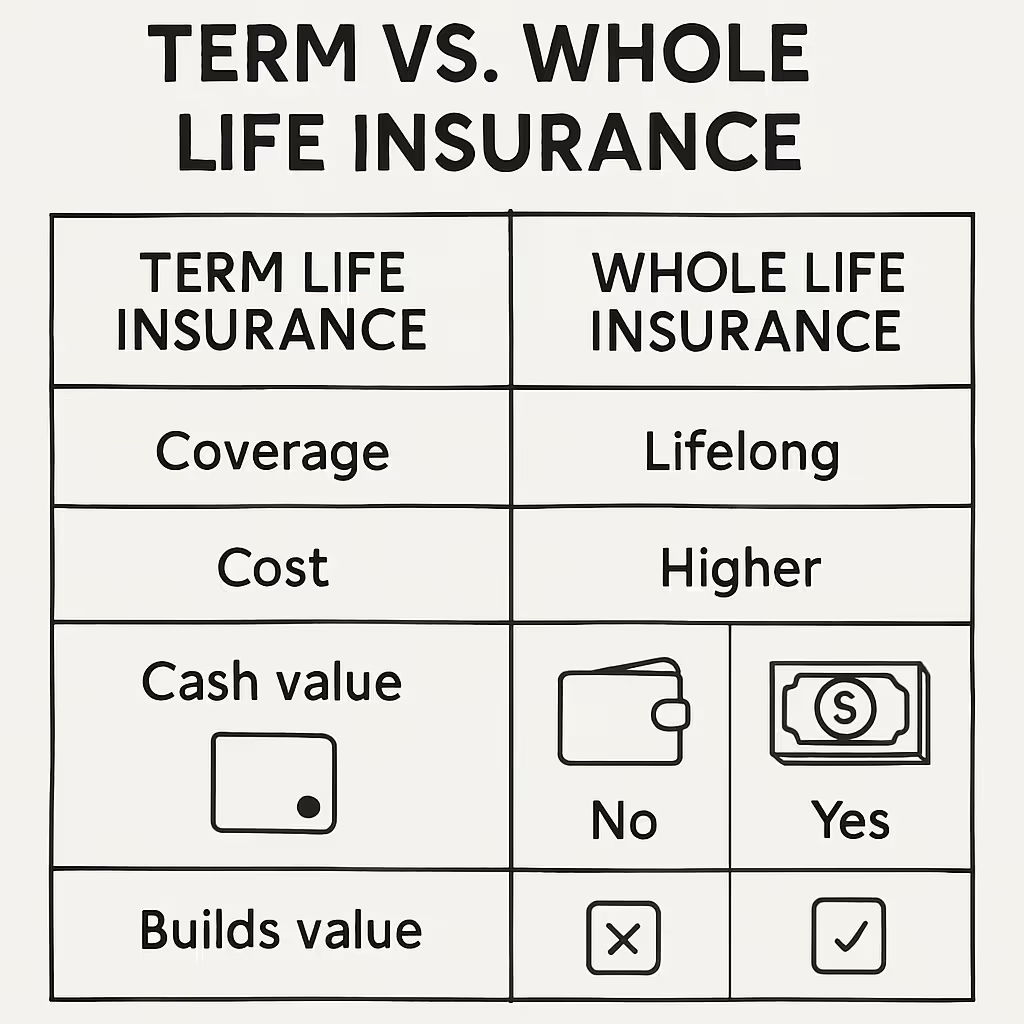

A fair commission structure for life insurance agents typically provides a high first-year commission (FYC) between 60% and 110% for term and whole life products, paired with renewal commissions of 2% to 5% for a set period. It should reward the agent’s expertise and the time spent providing personal guidance while maintaining the agency’s profitability.¹

For independent agents, “fairness” is usually measured by the level of support the IMO provides. If an agent is paying for their own leads (often 30% to 50% of their total expenses), they expect a higher contract level. However, at Life Policy Express, we emphasize the value of personalized service and real-time support. A competitive structure in 2026 might look like this:

Renewal commissions are a powerful but often overlooked way to keep agents loyal. While first-year commission rates get all the attention, it’s the agents who build strong renewal income who stick around. According to Insurance Business, life insurance agents typically receive a high commission on first-year premiums, ranging from 40% to 120%, but their renewal commissions decrease substantially to just 1% to 2%. As a result, renewal compensation is usually a smaller portion of an agent’s long-term earnings, which may impact retention strategies. Steady income from old policies shows agents that it pays to stay with you rather than chase slightly better deals elsewhere.

A good renewal commission plan signals to your agents that you want a long-term partnership. Here are certain key ways to design it:

To structure bonuses effectively, you must tie variable pay to key performance indicators (KPIs) like persistency, production volume, and multi-line sales. Performance-based bonuses should trigger when an agent reaches a specific premium milestone or maintains a persistency rate of 85% to 90%.

Effective bonus tiers include:

The best pay plans in 2026 are built on transparency, compliance, and automation. Give your agents a real-time dashboard that shows their earnings and renewals at a glance. This reduces confusion and keeps your top agents from looking elsewhere.

By focusing on a personalized, client-first approach, you can build a compensation plan that not just pays but also empowers your team to provide the clear, confident guidance for which Life Policy Express is known. Agents who feel fairly compensated and genuinely supported become your most effective recruiting asset, organically expanding your distribution footprint through word of mouth. In a competitive recruiting environment, a well-documented, easy-to-understand compensation plan is a differentiator in itself. Publish it clearly, explain it proactively, and revisit it annually to ensure it keeps pace with present market benchmarks and carrier incentive programs.