Discover the 8 key factors—from age and health to lifestyle and policy type—that affect your life insurance premium. Learn how to shop smart and lower your rate.

Two neighbors. Same age. Both are in decent shape. Both are non-smokers with steady careers. One opens her life insurance quote and breathes a sigh of relief. The other opens his and does a double-take. His rate is nearly 40% higher for the exact same coverage amount.

Sound familiar? It happens every day, and it is not random. Life insurance companies use a detailed process called underwriting to calculate what they call your mortality risk: the statistical probability that they will have to pay out your policy during the coverage period. Every data point they collect about you feeds that calculation. The higher the perceived risk, the higher the premium.

Here is the good news. Once you understand the 8 key life insurance premium factors, you can stop guessing and start planning. You will know which factors you can improve before applying, which ones require you to shop smart across multiple carriers, and how to build a policy structure that protects your family without overpaying. That is what this guide is here to help you do.

Some factors are baked in from the start. You cannot change them, but you can understand how they shape your quote and plan around them.

Age is the single most heavily weighted variable in life insurance pricing factors. The younger you are when you apply, the longer your statistical life expectancy and the lower the insurer's risk of a payout during your coverage period.

Think of it this way: a 28-year-old locking in a 30-year term policy is statistically very unlikely to pass away before that policy ends. A 55-year-old applying for the same policy represents a meaningfully different risk profile, and the premium reflects that.

Real-world example: A non-smoking professional in their mid-30s who purchases a 30-year term policy today will pay a substantially lower monthly premium than a colleague in identical health who waits until their mid-40s. Even a 10-year delay can translate into a major cost difference over the life of the policy. Buying early is one of the simplest ways to save money on coverage.

On average, women in the United States live roughly 5 to 7 years longer than men. Because a longer life expectancy reduces the insurer's payout risk over any given coverage period, women typically receive lower premiums than men with otherwise identical profiles.

The difference varies by carrier and policy type, but it is a consistent variable in traditional underwriting models across the industry.

Underwriting practices are evolving, and so is the conversation around gender. Transgender and non-binary applicants may face considerable variation across carriers in how gender is factored into their risk evaluation. Some insurers are moving toward more flexible approaches, allowing applicants to be rated based on their identified gender or current health profile rather than birth sex.

If this applies to your situation, working with an independent broker who understands carrier-specific policies on inclusive underwriting is strongly recommended. Practices vary considerably by insurer and state, so checking directly with each carrier is essential.

Health-related factors carry enormous weight in underwriting. These are the areas where proactive choices before you apply can make the most considerable difference to your rate.

Your physical health at the time of application is one of the most direct drivers of what affects life insurance premiums. For most traditional policies, this means a medical exam. Here is what insurers are typically looking at:

Chronic conditions such as Type 2 diabetes, heart disease, or high blood pressure signal a higher risk and typically result in elevated premiums or modified coverage terms. A BMI within a healthy range, along with well-managed vitals, generally supports a stronger underwriting classification.

Real-world example: An applicant in their mid-40s who has managed controlled Type 2 diabetes for several years will generally receive a higher rate than a comparable applicant without that diagnosis. That said, well-documented health management and a strong relationship with a primary care physician can help. Some carriers are more favorable toward applicants with stable, controlled conditions than others, which is exactly why comparing multiple carriers matters.

Tobacco use is one of the most significant factors that determine life insurance cost. Smokers and regular tobacco users can pay substantially more than non-users. The rate difference reflects decades of actuarial data linking tobacco to reduced life expectancy.

The category is broader than most buyers realize. Cigars, chewing tobacco, vaping products, and even nicotine patches are typically disclosed on applications, and many insurers screen for cotinine, a nicotine metabolite, during the medical exam.

If you have quit tobacco, the good news is that you may qualify for lower premiums. Most carriers require at least 12 to 24 months of being tobacco-free before reclassifying you as a non-smoker. The nuance worth knowing: applying for new coverage after quitting means going through underwriting again, which can sometimes surface unrelated health changes. Discuss the timing with a licensed advisor before making that move.

Even when your personal health is excellent, your family's medical history can still factor into your premium. Insurers look at first-degree relatives, meaning your parents and siblings, for patterns of hereditary conditions that may indicate elevated risk for you. Common red flags include:

A notable family medical history does not automatically price you out of good coverage. Carriers weigh this information differently, and many applicants with significant family histories still qualify for competitive rates. This is an area where shopping across multiple carriers through a knowledgeable broker can make a real dollar difference.

A history of therapy for situational stress, life transitions, or mild anxiety typically has little to no impact on your premium with most carriers. Insurers recognize that seeking mental health support serves as a sign of responsible self-care, not a liability.

However, a documented history of severe depression requiring hospitalization, a serious psychiatric diagnosis, or ongoing treatment for conditions such as bipolar disorder may affect underwriting outcomes. The degree of impact relies on the specific condition, how well it is managed, the length of time since any acute episodes, and the carrier's specific guidelines.

The most important thing is full transparency on your application. Omitting mental health history is not a shortcut to savings. It creates grounds for a claim denial when your family needs the payout most. An experienced independent broker can help you identify carriers whose underwriting guidelines are most favorable for your specific situation.

Your daily choices and activities tell underwriters a story about how you live and, statistically, how long you are likely to live. These factors are largely within your control, which means understanding them gives you real leverage.

Certain professions involve daily exposure to hazardous conditions, and life insurance rates reflect that. Jobs with elevated occupational mortality data, including firefighting, logging, commercial fishing, underground mining, and professional aviation, often carry premium surcharges.

The degree of impact rests on your particular role within the profession. A commercial airline pilot typically faces a different set of assessments than a crop duster. A construction project manager may be viewed differently from a roofer. Being specific about your actual duties when applying helps confirm accurate pricing and avoids surprises later.

Thrill-seeking hobbies introduce a statistically measurable risk of accidental death, and insurers account for them. Activities that commonly trigger premium surcharges or policy exclusions include:

If a hobby is seasonal, infrequent, or conducted under certified supervision, some carriers will treat it more favorably than others. Accurate disclosure is essential, and comparing how different carriers handle your specific activities is one of the best arguments for working with an independent broker rather than going direct to a single carrier.

Your driving history is a window into your risk tolerance. A record that includes DUIs, reckless driving convictions, or multiple moving violations within a short period signals behavior patterns that underwriters take seriously. This is a factor in how insurers calculate life insurance rates that many buyers overlook until they see their quote.

International travel is another consideration. Frequent trips to countries classified as high-risk due to active conflict, political instability, or elevated crime rates can add to your premium or trigger exclusions for deaths occurring in those regions. If you travel internationally for business, discuss this proactively with your broker before applying.

Real-world example: An applicant with a DUI conviction within the past three years will typically receive a meaningfully higher premium than a comparable applicant with a clean driving record, even if all other health and lifestyle factors are identical.

Beyond your personal profile, the policy structure you choose directly affects your premium. These are decisions you make, which means they offer some of the clearest opportunities to manage your costs.

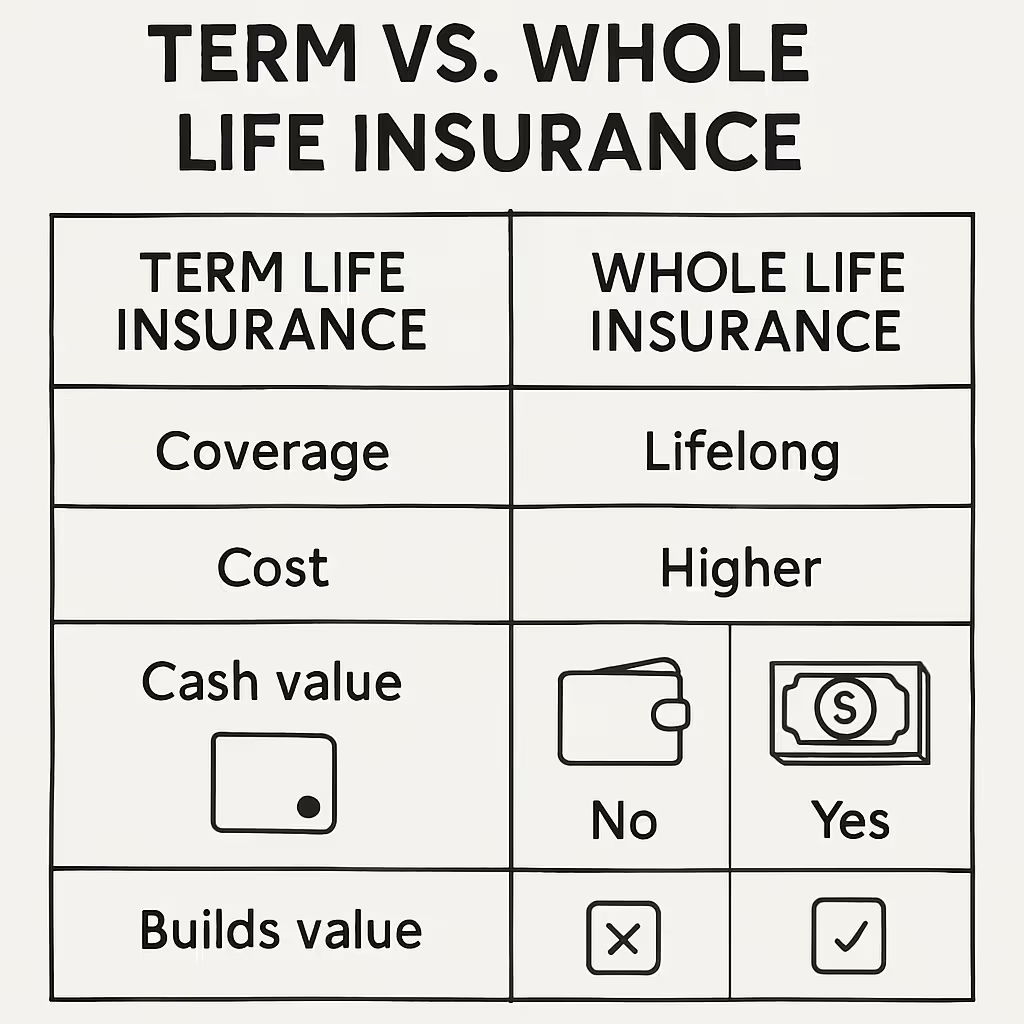

Term life insurance covers you for a defined period, typically 10, 20, or 30 years. Because the coverage is temporary and there is no cash value component, term policies are the most affordable option for the vast majority of buyers.

Permanent policies, including whole life and indexed universal life (IUL), provide permanent coverage and build cash value over time. These features come at a meaningfully higher premium for the same death benefit amount. For many families, the right starting point is a term policy during their highest-need years, with an option to revisit permanent coverage as financial conditions change.

The death benefit you choose is one of the clearest cost levers available to you. A larger death benefit means a larger potential payout for the insurer, which in turn translates into a higher premium.

The goal is not to buy as much coverage as possible. It is to buy the right amount. Working with an advisor to calculate your family's actual financial needs, factoring in income replacement, mortgage payoff, education costs, and existing savings, helps you land on a number that provides real protection without overpaying.

Riders are add-ons that expand the coverage of your policy. Common examples include:

Each rider increases your base premium. Some are genuinely valuable for your specific situation. Others may duplicate coverage you already have through your employer or a separate policy. Review each one carefully with your advisor rather than accepting the default bundle offered by a single carrier.

Buyers who prefer to skip the medical exam can apply for no-exam life insurance, also known as simplified issue or guaranteed issue coverage. The trade-off is predictable: faster approval and easier access in exchange for higher premiums and, in some cases, lower maximum coverage amounts.

For young, healthy applicants, traditional fully underwritten policies almost always produce better rates. For older buyers, those with health challenges, or those who simply need coverage in place quickly, no-exam options are worth evaluating alongside traditional coverage.

Understanding what affects your rate is the first step. Acting on that knowledge is what actually saves you money. Here are five strategies that work:

When clients walk in with layered profiles, such as a construction foreman who also competes in motorsports on weekends, or a 52-year-old with a family history of early cardiac events, your ability to move quickly and precisely across multiple carriers is what separates a placed case from a lost one.

Life Policy Express is built for exactly these occasions. The platform helps agents instantly compare quotes across diverse carriers, so you do not have to work case by case when applicants have complex health or lifestyle profiles that do not fit neatly into standard underwriting tiers.

The market has evolved faster than most training programs. Life Policy Express equips agents with educational resources designed to fill those gaps: mental health underwriting considerations, no-exam policy comparisons, and inclusive underwriting guidance for LGBTQ+ applicants. Knowing how to handle these conversations marks you as a comprehensive advisor, not just a quote generator.

One of the most powerful things you can do for a client is make the cost of their choices concrete and visible. When a client can see the exact premium difference between a term and a whole life policy, or understand precisely how a rider changes their monthly payment, the conversation shifts from abstract to actionable. That clarity creates trust and accelerates decisions.

Some of what affects your life insurance premium, specifically your age and your genetics, are outside your control. A lot of it is not.

Your tobacco use, your health metrics, your driving record, your hobby disclosures, and the policy structure you select are all decisions that directly shape what you pay. And how you shop for coverage, whether you go direct to one carrier or work with an independent broker who can compare across many, determines whether you find the best available rate for your actual profile.

Two things are non-negotiable. First, be completely honest on your application. Misrepresenting or omitting information is not a strategy. It is a risk that puts your family's payout in jeopardy at the most critical moment. Second, take the time to calculate your actual coverage need before you buy. Over-insuring costs you money every month. Under-insuring leaves a gap your family cannot afford.

Start with clarity on what you need. Work with a licensed advisor who can honestly compare your options. And if you are ready to see real numbers based on your real profile, Life Policy Express is here to help you do exactly that, free of pressure and without the runaround.

Age and current health status carry the most weight. Tobacco use is also a major factor and can significantly increase your rate regardless of other health markers.

Age, gender, current health and BMI, tobacco and nicotine use, family medical history, lifestyle and behavioral risks, policy type and structure, and driving record or international travel patterns.

Common reasons include older age at application, tobacco use, elevated BMI, chronic health conditions, a high-risk occupation or hobby, recent driving violations, or choosing a permanent policy type with a large death benefit.

Yes. High-risk occupations such as firefighting, commercial fishing, and mining typically result in higher premiums due to occupational mortality data.

Yes. Quitting tobacco, improving health metrics before applying, buying coverage while young, switching to annual payments, and comparing quotes across multiple carriers are all effective strategies.

Typically, yes. Simplified issue and guaranteed issue policies offer faster approval in exchange for higher premiums and lower maximum coverage amounts. They are best suited for buyers who cannot qualify for traditional underwriting.

A history of hereditary conditions in first-degree relatives, especially early-onset heart disease or certain cancers, can influence your underwriting outcome. Carriers weigh this differently, which is why comparing across multiple companies matters.

Term life insurance is far more affordable because it covers a set period with no cash value. Whole life and other permanent policies cost more but provide lifelong coverage and a cash value that grows over time.