An Expert's Guide to Choosing Your Life Insurance Policy.

Hello, and welcome. If you’re reading this, you’ve probably found yourself staring at a computer screen, completely overwhelmed by life insurance terms. You’re not alone. As an insurance professional, I can tell you that the "Term vs. Whole" debate is the single most confusing part of this process for almost everyone.

The entire life insurance industry, with its hundreds of products, really boils down to two basic concepts. The easiest way to understand them is to stop thinking about insurance and start thinking about real estate.

You essentially have one choice: Do you want to "rent" your protection, or do you want to "own" it?

That’s it. That’s the core difference. One option is temporary and affordable (renting), and the other is permanent and builds equity (owning).

My goal here isn't to sell you one or the other. It's to walk you through how each one works, just like I would with a client in my office, so you can confidently decide which one is right for you and your family.

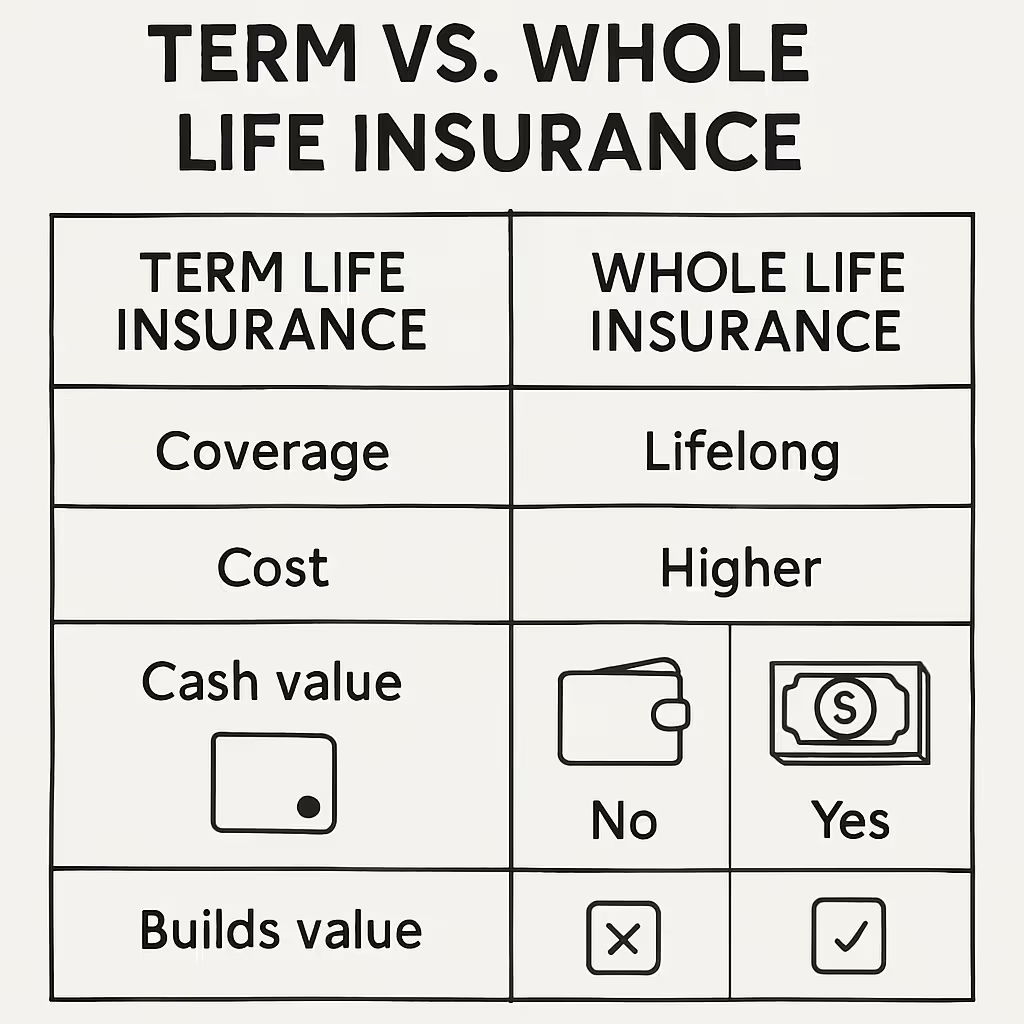

Term life insurance is the most straightforward and affordable type of insurance you can buy. It’s often called "pure life insurance" because that’s all it is—pure protection.

Here’s how it works: You "rent" a policy for a specific period, or "term"—typically 10, 20, or 30 years. You pay a fixed monthly premium. If you pass away during that term, the insurance company pays the full, tax-free death benefit to your family.

If the term ends and you're still living (which is what we all hope for!), the "lease" is up. The coverage simply expires. You stop paying, and the policy is over.

Who Is Term Life For?

This is the go-to solution for most young families, new homeowners, or anyone on a budget who needs a large amount of coverage for a specific period.

Think about your biggest financial responsibilities. They’re usually temporary:

Term life is designed to match these timelines perfectly. You can buy a $1,000,000 policy for a 30-year term to ensure that even if you're not there, the mortgage gets paid and your kids' college funds are secure.

The Pros:

The Cons:

Whole life is the most common type of "permanent" insurance. As the name suggests, it’s designed to cover you for your whole life.

This is the "owning" option. The premiums are higher, but in exchange, you get three powerful guarantees:

The "Expert" Feature: Understanding Cash Value

Think of cash value as a savings account or "equity" component built directly inside your life insurance policy.

With each premium payment, a portion pays for the cost of the insurance (the death benefit), and another portion goes into your cash value account. This cash value grows at a guaranteed, fixed rate, and it grows tax-deferred.

This cash value is an asset you can use while you are alive. You can take out policy loans against it or, in some cases, make withdrawals to help pay for college, supplement your retirement income, or handle an emergency.

A Quick Note on Policy Loans: When you borrow from your cash value, you're not really taking your own money out. You're taking a loan from the insurer with your cash value as collateral. The pros are that there's no credit check, the interest rates are typically low, and it's tax-free. The "catch" is that any loan you don't repay will be deducted from the final death benefit your family receives.

What About Dividends?

Many whole life policies are "participating" policies, which means you may also receive dividends. These are not guaranteed, but they're paid when the insurance company performs well. You can take them as cash, but most people use them to "buy paid-up additions," which is a fancy way of saying they use the dividend to buy more permanent insurance, which in turn grows more cash value and a larger death benefit.

The Pros:

The Cons:

You'll also hear about "Universal Life" (UL). Think of this as another type of "owning". The main difference between Whole Life and Universal Life is flexibility.

This flexibility can be great, but it also means the policy requires management. If you don't pay enough into it, or if interest rates are low, your policy could be in danger of lapsing. It’s a more advanced tool, whereas whole life is built for stability.

So, how does this apply to real people?

Scenario 1: The New Parents

Scenario 2: The Legacy Planner

Scenario 3: The "Best of Both" Strategy

Riders are optional add-ons that enhance your policy's coverage. Here are three you should always ask about:

You can get an online quote for life insurance in 30 seconds. And for a simple term policy, that might be fine. However, an online form can't ask you about your goals, business, legacy, or strategy. It's programmed to give you the cheapest price, not the best plan.

The goal is to find the right tool for the right job. Term life is a fantastic, affordable tool for income and debt protection. Whole life insurance is an unmatched tool for creating a guaranteed, permanent legacy and building wealth.

Now that you understand the difference, you can have a more confident conversation about creating the right plan for your family.