Find the best 5 final expense policies that accept seniors with health issues. Learn if burial insurance is worth it and secure clear, local advice.

Looking for end-of-life insurance when you have a chronic health condition can feel stressful. A lot of people believe that if you have heart issues, breathing problems, or diabetes, you will not be able to find an affordable policy. This idea can leave families with surprise expenses when they are already going through a tough time.

These days, there are insurance options designed for older adults. If you understand how insurance companies look at health risks, you can find good coverage without medical exams or dealing with pushy salespeople.

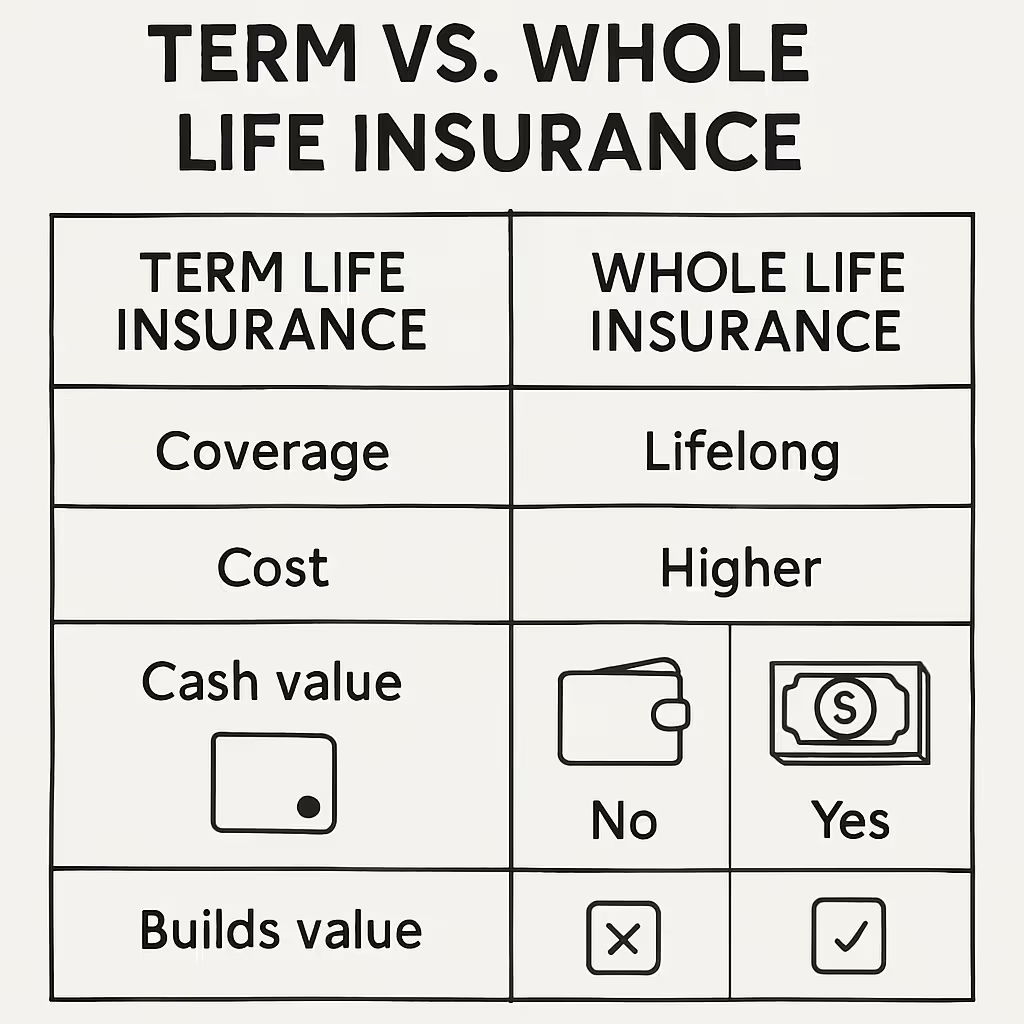

Final expense insurance is a kind of whole life policy with a smaller payout. It is there to help with funeral costs, cremation, medical bills, and other end-of-life expenses. The policy builds a small cash value, your payments never go up, and your loved ones receive the money tax-free.

Unlike bigger life insurance policies that require large payouts and medical exams, these plans are simple and easy to get. The coverage is usually a few thousand dollars, which helps families pay for the funeral or cremation they choose without buying more insurance than they need.

Yes, you can still get final expense insurance even if you have health problems. Depending on your health, you might qualify for a plan that pays the full benefit right away, or one that has a short waiting period before the full amount is available.

Insurance companies do not expect perfect health. They look at how stable your conditions are, how long ago you had any major health events, and what medicines you take. That is why there are different types of policies for different health situations.

For seniors with well-managed chronic conditions, simplified issue whole life insurance provides the most competitive route. These applications replace physical medical exams with a concise series of yes-or-no health questions. If you can answer no to critical conditions like current hospitalization, terminal illness, or active cancer treatments, you can secure first-day full coverage. This tier represents a highly efficient mechanism for seniors who manage diabetes or mild hypertension but are otherwise stable.

If you have had a serious health event in the last year or two, like a stroke or heart procedure, you might be offered a graded policy. This means you are approved, but the full payout is not available right away. If you pass away from natural causes during the first couple of years, your family gets back what you paid in, plus some interest.

For seniors facing significant, complex health challenges, guaranteed-issue life insurance plans completely eliminate medical underwriting. Because there are no health inquiries, acceptance is guaranteed solely on the age criteria. These contracts inherently feature a standard 24-month graded waiting period, serving as an essential financial safety net for individuals who cannot pass conventional medical screening.

When navigating final expense insurance with health issues, matching your exact medical history to the correct policy architecture is critical. Here are five distinct final expense policy styles designed to accommodate varying levels of senior health issues.

This is designed for applicants managing common health issues such as well-controlled high blood pressure or lifestyle-managed type 2 diabetes. This structure uses final-expense, no-health-questions forms for physical health, relying instead on automated medical index and pharmacy database sweeps. If no severe red flags appear, the policy issues with an immediate, full death benefit from day one.

Specifically made for seniors who take common maintenance medications for circulatory health or glucose control. Many top-tier carriers overlook diabetes entirely if it was diagnosed after age 40 and is not accompanied by vascular complications or insulin shock. While final expense insurance rates rise with age, purchasing a policy earlier helps lock in a lower premium that remains the same for the life of the policy, according to MoneyGeek. The Controlled Respiratory Care Policy

This policy is for people with breathing problems like mild asthma or stable COPD. If you do not need oxygen all the time, you can usually get full coverage right away. If your condition is more serious, you might need a graded policy.

This policy style serves as a transitional bridge for individuals who are recovering from serious health scares but are now medically stable. If an applicant experienced a stroke or heart attack, or underwent major vascular surgery, more than 12 months ago but less than 24 months ago, this framework delivers coverage without permanent declination, graduating to full protection once the look-back window closes.

This policy type represents the ultimate safety net for senior life insurance high-risk profiles. If an individual is currently managing advanced congestive heart failure, active cancer therapies, or neurological disorders, standard underwriting is unavailable. By using a pure final expense, no-health-questions blueprint, the applicant secures a permanent policy based solely on meeting the carrier's age parameters.

Yes, burial insurance is worth it for families who want to prevent sudden, out-of-pocket funeral costs from depleting household savings. It provides immediate cash liquidity, making sure that final arrangements, cremation fees, and outstanding medical balances are resolved without relying on expensive credit card debt.

End-of-life costs keep going up. The average funeral with a viewing and burial costs about $8,300, and a cremation with a viewing is about $6,280, based on data from the National Funeral Directors Association. When you add in things like cemetery plots and medical bills, families often end up paying more than $10,000 out of pocket.

For many families, coming up with $10,000 right away is just not possible. A final expense policy turns that high, unexpected cost into a small, steady monthly payment that fits into your budget.

Navigating the landscape of senior life insurance high-risk options does not require submitting your personal data to digital lead mills that bombard your phone with automated spam. The key to finding competitive rates lies in accessing personalized, multi-carrier guidance tailored to your state's specific guidelines.

Through Life Policy Express, you bypass generic call centers and connect directly with a licensed, local advisor. Your local professional reviews the exact. With Life Policy Express, you skip the call centers and talk directly to a licensed advisor in your area. They will review your health history and identify the insurance company that offers you the best chance of approval. This way, your family gets real financial security without any sales pressure or confusion.