Stop guessing how much life insurance you need. Learn the DIME method (Debt, Income, Mortgage, Education) and the critical factors (unpaid labor, inflation, debt) most online calculators miss to find your family's true coverage gap.

Most people know they should get life insurance, but it is hard to feel sure about the right amount. How much is enough? What if you do not buy enough and your family is left unprotected? What if you buy too much and pay for coverage you do not need? These questions do not mean you are careless with money. They show you are taking a tough decision seriously.

The numbers behind the gap are sobering. According to LIMRA’s most recent data, roughly 52% of American adults have some form of life insurance, yet 41% of those insured admit they do not have enough coverage. Separately, 44% of U.S. households say they would face financial hardship within 6 months of losing their primary earner, and 28% would reach that point within 1 month.

The real issue is not that you cannot find calculators or simple rules. The problem is that these tools only show part of your family’s real financial needs. In this post, I will walk you through the formulas that actually help, point out the hidden costs people often miss, and show when it makes sense to get advice from a licensed professional.

Before you start personalizing, it helps to use a solid structure. Insurance professionals often use three main formulas, each with its own strengths.

The easiest way to start is to multiply your yearly salary by 10-15. For example, if you make $75,000 a year, you would consider coverage between $750,000 and $1.125 million. This is a quick estimate, but it misses some big things like debts, future college costs, or the value of a spouse who does not earn a paycheck.

The DIME method is a more disciplined framework that financial professionals frequently recommend as a baseline. DIME stands for:

For example, a family with two young kids, a $280,000 mortgage, $40,000 in debt, a $120,000 household income, and plans to pay for two college educations would need between $1.9 million and $2.3 million using the DIME method. This number surprises many people, which is why using a formula is better than guessing.

The Human Life Value method considers your future earning power rather than just your current bills. As a rule of thumb, it suggests about 30 times your income if you are in your 30s, 20 times your income in your 40s, and 10 times your income in your 50s.

For example, if you are 38 and earn $90,000 a year, the HLV method would suggest about $2.7 million in coverage. This may sound high, but it shows how much income your family would lose over your working years.

Standard formulas are a starting point, not a finish line. Several real-life variables consistently fall through the cracks of generic life insurance needs calculators, and each one can meaningfully change your coverage target.

Think about a family where one parent works and the other stays home to handle childcare and everything else. If the stay-at-home parent passed away, the other parent would suddenly have to pay for childcare, tutoring, meals, and household expenses. Studies show that replacing all this work can cost over $100,000 a year. You should include this in your coverage amount.

A significant and growing share of middle-aged adults find themselves simultaneously supporting their own children and caring for aging parents. If you are in this position, your life insurance coverage amount needs to account not only for your children’s needs but also for the long-term or assisted living expenses your parents may depend on you to help fund. Failing to include these obligations creates a serious gap that only becomes visible at the most unfortunate moment.

Most online life insurance calculators are made for people with regular jobs. If you own a business, freelance, or work for yourself, things get more complicated. Business loans, keeping the business running, and buy-sell agreements are all extra financial risks your family or business partner could face. You might need a separate key person policy in addition to your personal coverage.

The DIME method uses $100,000 to $150,000 per child for college, but that is based on today’s prices. College costs have increased by about 22% every 10 years. If you have a newborn, you should plan for education costs that are 40% to 50% higher, which could mean adding $50,000 to $75,000 or more per child to your coverage.

After you figure out your total coverage need, the next step is to subtract the resources your family could actually use if something happened to you now.

You can subtract liquid assets like savings, brokerage accounts, and education savings plans from your coverage to find your real gap. Do not subtract retirement accounts, such as a 401(k) or IRA. These have penalties and taxes if you take money out early, so your family cannot count on them for daily expenses. Treat them as long-term savings, not emergency money.

About 60% of U.S. employers offer group life insurance. This might seem like a good safety net, but group coverage usually ends when you leave your job, whether you quit, get laid off, or have to stop working for health reasons. It is best to view employer coverage as an extra, not your main policy. Relying only on work benefits can leave your family without coverage when they need it most.

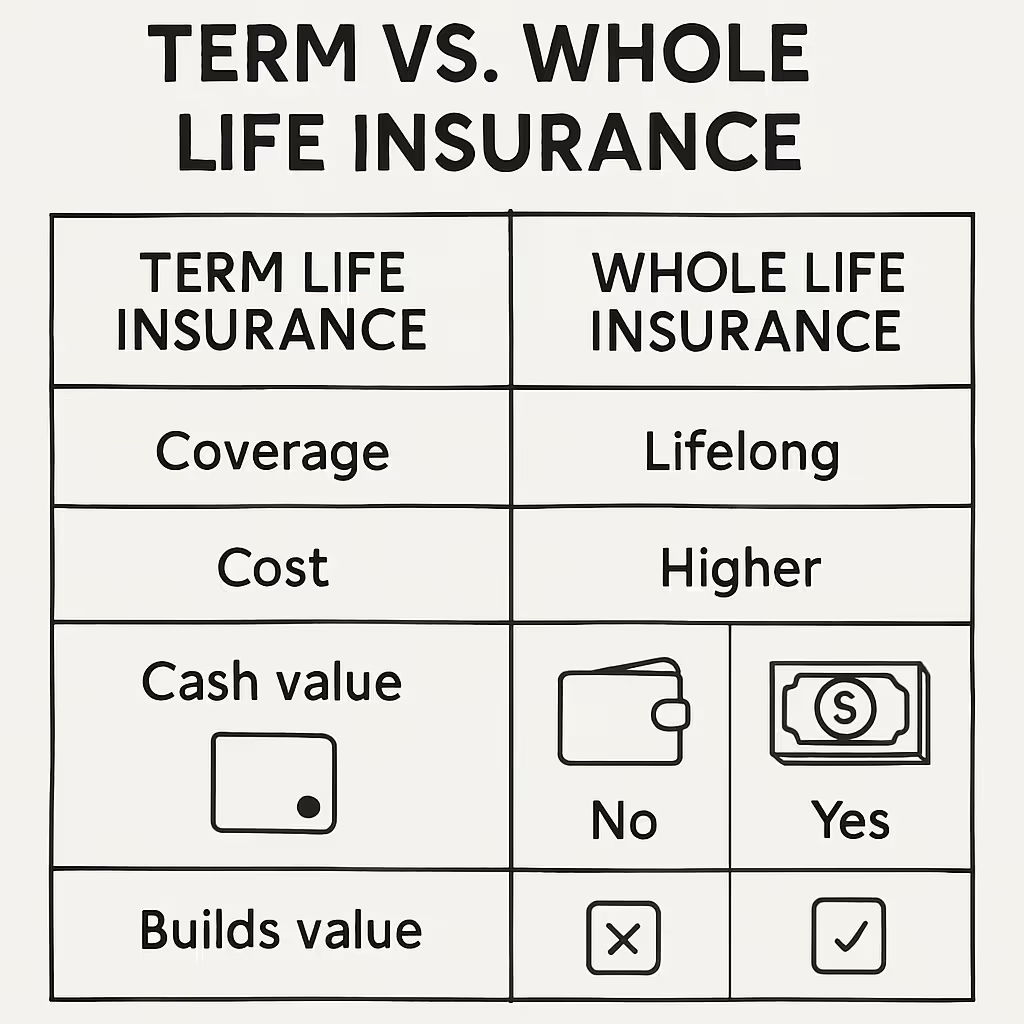

Knowing how much life insurance you need is only half the equation. The other half is choosing the product structure that fits your goals and budget.

Rather than purchasing a single large policy, a laddering approach consists of stacking multiple term policies with different durations. For example, a 10-year term policy might cover the years until the youngest child graduates college, while a 20-year term policy handles the remaining mortgage balance. When the 10-year policy expires, the overall premium cost drops substantially. This approach allows for more targeted coverage at a lower total cost than a single large policy would.

Many term policies let you convert to a permanent policy later without a new medical exam. This is helpful if your health changes during the term. It gives you the option to keep permanent coverage no matter what happens with your health.

There is a meaningful gap between what online calculators can deliver and what a family actually needs. Most people who sit down with a generic life insurance calculator walk away either confused by the output or confident in a number that does not reflect their complete situation. They may overestimate the cost of coverage and delay action altogether. Or they may buy a policy that looks adequate on paper but leaves critical obligations uncovered.

This is the gap that licensed insurance professionals are uniquely positioned to fill. At Life Policy Express, agents have access to a platform that connects them with buyers who have moved beyond casual browsing and are actively looking for expert guidance. A client who has already completed a DIME calculation and is still unsure of their number is not a cold lead. They are a motivated buyer who needs a professional, not another calculator.

The details that fall through the cracks of automated tools, including the value of a stay-at-home spouse, the specific obligations of a business owner, or the compounding effect of inflation on education costs, are exactly the areas where a knowledgeable agent can add measurable value. By participating in these conversations as a trusted consultant rather than a salesperson, agents build long-term client relationships that generate referrals and repeat business for years.

Life insurance is not something you decide once and forget. It is part of your financial plan and should be reviewed whenever big life changes happen. Getting married, having a child, buying a home, starting a business, or approaching retirement are all times to review your coverage.

The formulas in this post, from the straightforward 10x income rule to the more precise DIME method, give a structured starting point for determining the right amount of life insurance coverage. But formulas work with numbers, not with your family’s specific circumstances, values, and goals.

If you have done these calculations and still feel unsure, or if your situation is more complicated, the best next step is to talk with a licensed professional. They can review your needs and help you find the right coverage for your life.