Making Life Insurance Less Complicated and More Meaningful.

As a licensed agent, I’ve spent my career having some of life’s toughest conversations. Nobody wants to talk about life insurance. It’s not fun, and it forces us to think about a future our loved ones might have to face without us.

I see the same hesitation every day. It’s not just you. It’s a completely human trait to put this conversation off. We’re all wired with a “normalcy bias”—a deep-seated, healthy belief that our lives will continue tomorrow just as they did today. We also have a powerful “optimism bias,” that little voice in our head that says, “It won’t happen to me.”

These feelings are normal. But they’re often supported by a rational-sounding excuse: “It’s too expensive.”

Let me be clear: this is the single biggest misunderstanding about life insurance. Studies show that the majority of people, especially younger people, wildly overestimate the true cost. They assume it's out of reach, so they put it off, always finding “other priorities” that feel more immediate.

The truth is, for a young, healthy person, a meaningful policy is often incredibly affordable.

If you’re wondering whether this article is for you, ask yourself one simple question: "If I were to pass away, would anyone I love face a financial hardship?"

It’s that simple. If the answer is yes—if you have a spouse, a child, a business partner, or even aging parents who rely on you—then the conversation is no longer optional. It’s a responsibility. The question isn't if you need it, but how to get the right protection in place.

My job isn't to sell you a product. It's to help you build a plan. Let’s do it together.

The first thing I hear from most people is, “I’m all set. I have it through work.”

While group life insurance from an employer is a fantastic perk, it’s just that: a perk. It’s a great supplement, but it should never be your family’s entire strategy.

Here's why. The "free" or low-cost insurance you get from work has three major flaws:

The real danger is that this group policy gives you a false sense of security during your youngest, healthiest years—the very years when insurance is most affordable. If you rely on it for 20 years and then leave your job at 50, you'll be shopping for a new policy. But you'll be 20 years older, and perhaps you've developed a health condition. What was once affordable may now be 10 times the price, or you may not be able to qualify at all.

You need a foundational policy that you own. One that is not tied to your job. One that locks in your good health today and can't be taken away from you, no matter where your career goes.

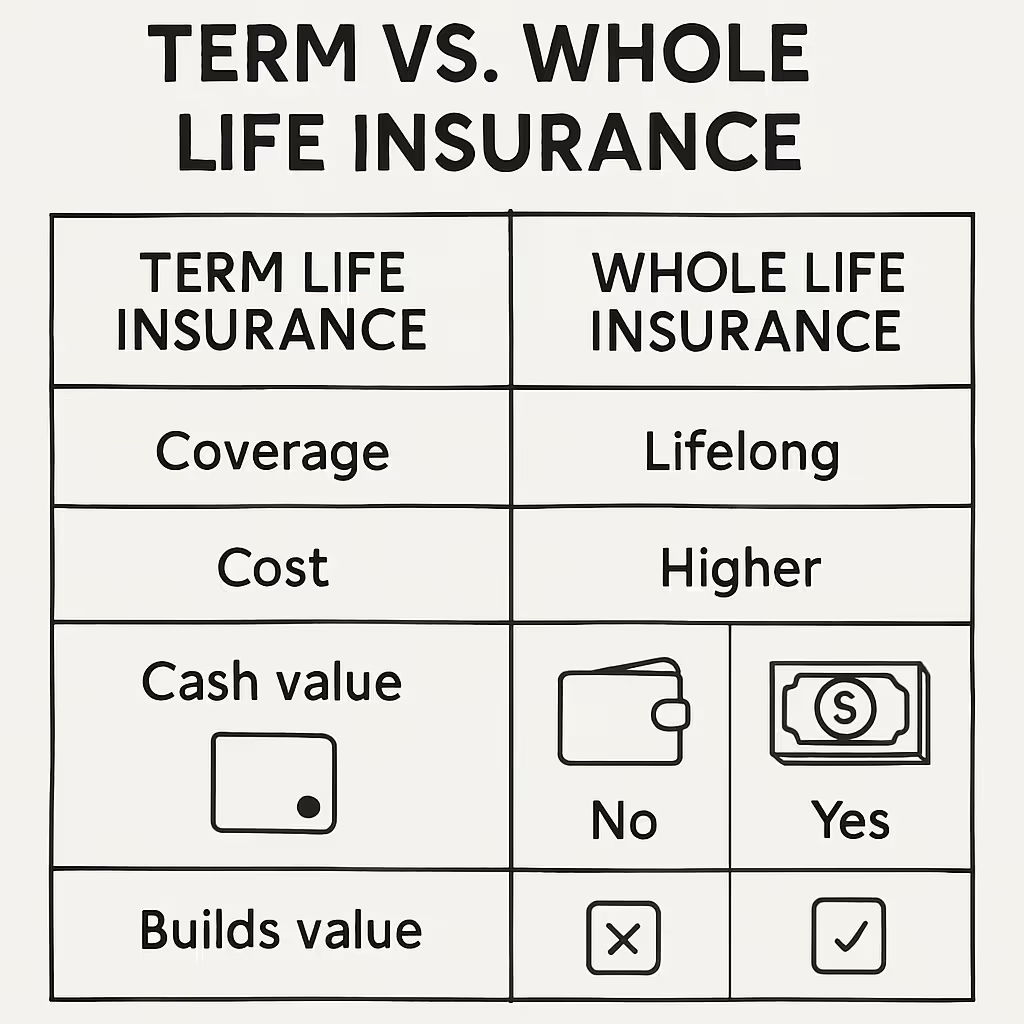

This brings us to the most fundamental (and most confusing) choice: Term or Permanent?

All the different product names you hear—Whole Life, Universal Life, Term—really boil down to two basic concepts. The easiest way to understand them is by using the "rent vs. buy" analogy.

Term life insurance is like renting an apartment. It is “pure life insurance.” You select a "lease" period—typically 10, 20, or 30 years—and you pay a fixed premium for that time.

Permanent life insurance (like Whole Life) is like buying a home. It's more of an upfront commitment, and the premiums are higher, but it's yours for your entire life. As long as you pay the premiums, the policy is guaranteed.

The internet loves to frame this as a "Term vs. Permanent" fight. As an agent, I see it differently. They are two different tools for two different jobs.

Here’s the strategy I build with most of my clients: it's not a single policy, it's a plan. We "stack" them. We use an affordable "rented" Term policy for the big, temporary "what-ifs"—paying off the mortgage and replacing income. Then, we pair it with a smaller, "owned" Permanent policy that will last forever. This permanent piece will cover final expenses, so your family never has to worry about that, and it will build cash value. You get the best of both worlds: affordability for your big needs now, and a guaranteed foundation for life.

"How much do I need?" is the next big question. You've probably heard the old rule of thumb: "10 times your income."

That’s a decent starting point, but it's a guess. It doesn't take a detailed look at your family's actual needs. Does that 10x include your $400,000 mortgage? Your $50,000 in student loans? Probably not. This is why so many people are underinsured.

In my office, we do a quick needs analysis to find your real number. You can do a simple version of this right now. It's called the D-I-M-E method.

Add up D + I + M + E. That total is your "peace of mind" number. It’s not a guess. It’s the exact amount of money it takes to make sure your family's life can go on, in the home they love, with the future you always planned for them.

You can run all the numbers you want, but the impact of this decision never hits home until you see what happens when it's too late.

I'll change the names, but this story is one I’ve seen versions of too many times. "Mark" and "Sarah" were in their late 30s. They had two young kids, a new mortgage, and a busy life. Life insurance was on their "to-do" list, but other priorities always seemed more urgent.

Mark was killed in a car accident on his way home from work.

Sarah’s grief was instantly compounded by financial panic. Within 48 hours, she discovered two things: their savings were minimal, and Mark’s group policy from work was only $50,000.

The funeral home needed $9,000 upfront. She didn't have it.

I watched, helpless, as her family had to create a GoFundMe page. They were forced to make their private grief public, asking for donations from friends and strangers just to give Mark a proper memorial.

The $50,000 from his work policy was gone in an instant—it covered the funeral and a few months of bills. And then, the mortgage payment was due. Sarah's income alone couldn't cover it.

This is the true tragedy. The lack of planning didn't just leave her with bills; it stole her time to grieve. She was thrust into a financial struggle, forced to make massive, life-altering decisions while she was still numb.

Now, let me tell you about the other side of my job. The part that is, in its own way, sacred. It's when I have to visit a grieving family, but this time I'm carrying a check. That check, which we calculated using the DIME method, pays off the mortgage. It funds the college accounts. It keeps the lights on.

It doesn't remove the pain. Nothing can. But it removes the panic. It buys that family what they need most: time. Time to heal, together, in their own home, without a single financial worry. That is the "impact" of this piece of paper.

A modern life insurance policy is more than just a check for when you're gone. Some of the most valuable features are the ones that protect you while you're living.

These are called "riders," and they’re like optional features you can add to your policy "chassis" (the Term or Perm) to make it fit your life perfectly. A good agent will ask you about these; a simple online form won't.

Here are the three "impactful" riders every family should ask about:

In a world of "quick, easy and cheap" online ads, it's tempting to treat life insurance like a commodity. It’s not.

The cheapest policy you find with a click may not be the best option. It might be from a company with a poor claims-paying history, or it may be a bare-bones policy missing the critical riders we just discussed.

An online form can't do a "personalized needs assessment." It can't ask you follow-up questions. It can't listen. A computer will give you the cheapest price; a licensed agent will work with you to find the best value.

My value to my clients isn't just in the setup. It's in the long-term relationship. As your life changes—you have another child, you buy a new house, you get a promotion—we'll meet to review and adjust your plan to make sure it's always working for you.

But here is the most important point of all: When the unthinkable happens, who do you want your grieving spouse to call? A 1-800 number for a website, or a person they know and trust?

My job isn't to sell you a policy. My job is to be the first call your family makes. My job is to handle the paperwork, to be their advocate, and to make sure the promise we put on paper today is fulfilled.

That's the real "impact."

If you're ready to move this off the "to-do" list, let's have the conversation. Let's build your family's safety net, together.