How to Read a Life Insurance Policy (Without the Confusion)

Learn how to read a life insurance policy without the stress. Our guide translates complex legal jargon and highlights the key pages you need to review for total financial peace of mind.

April 16, 2026

X min read

Receiving a 50-page life insurance policy contract full of legal and financial terminology can feel incredibly overwhelming. Unless you work directly in the US insurance industry, all the specific clauses and subclauses might sound like a completely foreign language. As a result, many buyers simply stuff their new policy documents into a drawer without reading them. Unfortunately, this common habit can lead to denied claims, unexpected coverage lapses, or missed financial benefits for your family.

Our goal at Life Policy Express is to reduce buyer confusion and build brand trust by making insurance simple. In this guide, we will show you exactly how to understand a life insurance policy — translate the technical language of your contract into plain English, show you which pages matter most, and empower you to take total control of your financial protection.

Life Insurance Policy Sections — Where to Look First

You do not need to read your entire policy like a novel. Reading a life insurance policy becomes far easier once you understand the standard structure. Knowing the key life insurance policy sections will save you time and frustration.

The Declarations Page (Cover Page): Think of this as the executive summary of your coverage. Usually found in the first few pages, the declarations page lists your basic but critical information: the policyholder's name, the death benefit amount (sometimes called the face amount), the premium cost, the policy number, and the policy issue date. Review this page immediately to ensure your personal details are entirely accurate.

The Insuring Agreement: This section is the core of the contract in which the insurance company makes its official promise to pay the death benefit to your loved ones in exchange for your premium payments. It outlines the major details of what is covered and your rights as the policy owner.

Riders and Endorsements: These are customized, optional add-ons that give your base policy extra power. A policy rider such as the accelerated death benefit rider, waiver of premium rider, or child protection rider can significantly expand your coverage. Look closely to see what supplemental coverage you purchased.

Life Insurance Policy Terms Explained — Key Jargon Translated

Insurance contracts use a very specific legal vocabulary. To fully grasp your policy, you need to know the definitions of these key life insurance policy terms explained in plain English.

Beneficiary: The person, people, or entity designated to receive the death benefit payout when the insured passes away. It is critical to keep this updated after major life events such as marriage, divorce, or the birth of a child. For more detailed strategies, refer to our guide on life insurance beneficiary rules.

Grace Period: This built-in safety net keeps your coverage active if you accidentally miss a premium payment. Most states mandate that the grace period last for at least 31 days, giving you extra time to pay without losing your family's protection.

Free-Look Period: A trial period (typically 10 to 30 days) during which you can review your new contract and cancel it for a full refund with no penalty. Knowing what does the free look period mean in life insurance can save you from being locked into a policy that does not fit your needs.

Contestability Period: A specific window of time — usually the first two years — during which the insurer has the right to investigate and potentially deny a claim if it finds inaccurate information in your original application.

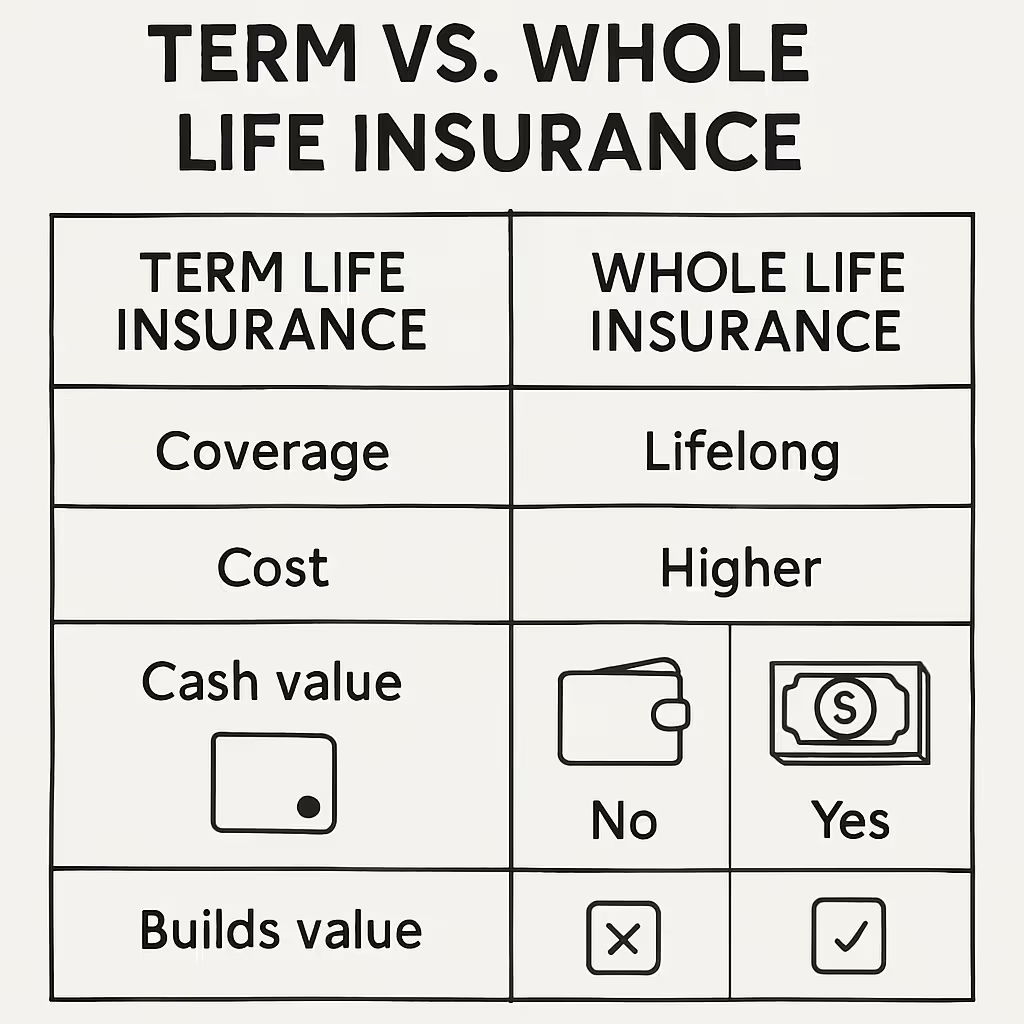

Cash Value: If you own a permanent life insurance policy (such as whole or universal life), it includes a wealth-building component known as cash value. This money grows over time and can be borrowed against or withdrawn during your lifetime. Term life insurance contracts do not build cash value.

For a complete breakdown of every term you might encounter, bookmark and visit our official insurance terms glossary.

What to Look for in a Life Insurance Policy Document

Knowing what to look for in a life insurance policy document can protect your family from unexpected surprises at claim time. Because many policies are now digital PDFs, use the Ctrl+F (Find) keyboard shortcut to navigate efficiently instead of reading page by page.

Search "Exclusions": Understanding life insurance exclusions and limitations explained is just as important as knowing what is covered. Policy exclusions highlight situations that invalidate a payout — frequent examples include a suicide clause during the contestability period, high-risk hobbies like aviation, or acts of war.

Search "Settlement" or "Claims": Locate the instructions your beneficiary will need to actually file a claim and receive the payout. Making sure your loved ones know the rules of this section can prevent major complications during an already difficult time.

Life Insurance Policy Declarations Page Explained — Illustrations & Inflation

If you purchased a permanent life insurance policy, your document will include a policy illustration. Understanding the life insurance policy declarations page explained section on illustrations means reading projections showing how your cash value and premiums could perform over time based on certain assumptions.

Guaranteed vs. Non-Guaranteed Values: Illustrations feature columns for both. Guaranteed values are the absolute contractual minimums the insurance company promises to provide. Non-guaranteed values are hypothetical projections based on assumed interest rates and market results. Never treat a non-guaranteed projection as a promise.

Focus on the Early Years: Many illustrations look fantastic in their 30s or 40s. However, look closely at the first 5 to 10 years — this is where fees, administrative costs, and policy efficiency are most visible. Cash value growth is rarely linear, so expect it to grow slowly in the early years.

Account for Inflation: Over 20 or 30 years, the purchasing power of your death benefit will decrease due to inflation. Check your policy to see if you have an inflation rider, which automatically increases your payout over time to help your coverage keep up with the rising cost of living.

Pro-Tips for Policy Management & Storage

Once you understand the details of your coverage, you need to manage and store it correctly. Here are a few expert best practices to ensure your policy protects the people who need it most.

Avoid the Safe Deposit Box Trap: Keep your physical policy documents secure, but avoid storing them in a bank safe deposit box. After a death, a person's assets are often frozen until the estate goes through probate. Since life insurance is designed to pay out immediately for short-term costs like funerals and daily bills, sealing it in a bank box can delay access. Keep a copy in a fireproof safe at home, or leave one with your attorney.

Create a Cheat Sheet: Take the burden off your grieving family members by creating a simple summary document. Log your policy numbers, the death benefit amounts, your premium due dates, and the contact information for your insurance agent. Store this cheat sheet where your family can easily find it.

The Backdating Hack: If you are currently applying for a new policy, ask your agent about backdating. Insurance companies calculate your insurance age based on your nearest birthday, effectively accelerating your age by six months. Many insurers allow you to backdate a policy up to six months to lock in a younger insurance age and secure a better premium rate.

What Are the Key Sections of a Life Insurance Policy?

What is the Difference Between a Rider and a Policy?

A life insurance policy is the core contract that defines the death benefit, premium, and all terms and conditions of your coverage. A policy rider is an optional amendment that modifies or supplements the base policy — for example, adding critical illness coverage or a child protection benefit. Think of the policy as the foundation and the rider as a custom upgrade.

How LifePolicyExpress.com Helps You Navigate Your Coverage

The tools at LifePolicyExpress.com are built to help both buyers and agents simplify the underwriting process and improve the client experience.

1-Page Express Summaries: Agents can use the platform to automatically generate visual, easy-to-read cheat sheets that summarize dense 50-page contracts. This builds instant trust and radical transparency between the agent and the buyer.

Digital Vaults and Easy Sharing: Agents can offer clients a secure digital storage solution that grants access to a designated beneficiary — removing the stress of tracking down physical paperwork.

Automated Review Reminders: The platform tracks major life events and triggers annual review reminders, ensuring your agent checks in regularly to adjust coverage, update your beneficiary list, or add new policy riders as your family's needs evolve.

Conclusion

A close, informed reading of your life insurance policy can make all the difference when your family needs financial protection the most. Knowing exactly what your terms mean, what is included in your coverage, and what is excluded helps you make confident financial decisions. When you truly know how to understand a life insurance policy, you put yourself in complete control of your family's financial future.

Take 15 minutes today to pull out your document. Verify your declarations page for accuracy, ensure your beneficiary designations are up to date, and locate your exact death benefit amount. If you spot an error or feel confused by the terminology, compare life insurance quotes and use the streamlined tools at LifePolicyExpress.com to translate the jargon. Your family's secure financial future is absolutely worth the effort. For deeper context, visit our complete guide to life insurance.

As President of Financialize and a licensed life insurance professional, he oversees a suite of modern financial platforms, including Life Policy Express, Annuities.net, and Lead Revival™. Over the last five years, he has established himself as an innovator in the industry, applying data-driven strategies to help agents succeed while ensuring consumers receive transparent, expert guidance on their financial future.