The definitive life insurance guide. Learn how to compare policy types (Term vs. Whole/IUL), calculate your coverage needs using the DIME formula, and secure your family's financial future. Start your comparison today.

Welcome to the definitive life insurance guide for 2026. If you are searching for a complete guide to buying life insurance online, you have found the right resource. We understand that exploring the financial protection space can feel overwhelming, especially with the vast amount of industry jargon. That is why this article focuses heavily on having life insurance explained for beginners. Our mission is to strip away the confusion and provide you with useful, experienced insights. Securing affordable life insurance is one of the most profoundly caring financial decisions you can make for your family. By the end of this resource, you will have the knowledge you need to protect your loved ones and build long-term generational wealth.

What is life insurance, and how does it work? A life insurance policy is a legally binding contract between you and an insurance company. You agree to pay regular premiums, and in exchange, the company promises to pay a tax-free lump sum of money to your loved ones when you pass away.

To clearly grasp how life insurance works, you must look at the three main components of the contract. First, there is the premium, the amount you pay monthly or annually to keep the coverage active. Second, there is the death benefit, the predetermined amount the insurance company will pay out. Finally, there is the life insurance beneficiary. Your life insurance beneficiary is the specific person, trust, or charity you legally designate to receive the death benefit. The funds can be used for absolutely any purpose, from covering immediate funeral costs to paying off a family mortgage or funding a child’s college education.

Understanding exactly how life insurance works entails accepting that it is essentially a risk transfer. You are transferring the financial risk of your premature death to an insurance carrier so that your family does not have to bear the economic burden alone. When you explain how life insurance works to a spouse or business partner, you can emphasize the incredible peace of mind it provides for your overall financial plan.

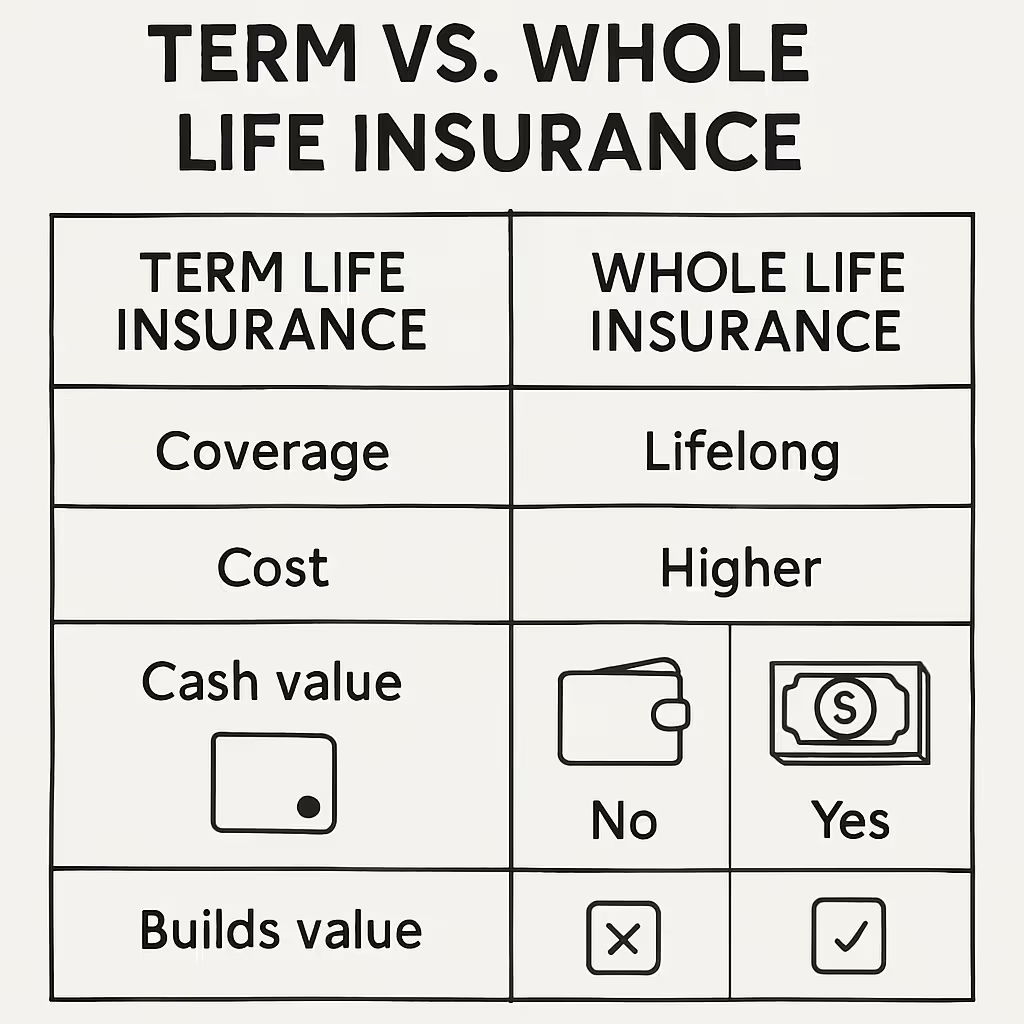

The different types of life insurance available today are designed to fit a wide variety of financial situations and goals. There is no single standard policy. Instead, the market is divided into two primary categories: temporary and permanent coverage. Exploring these types of life insurance will help you align your purchase with your family’s special needs.

A term life insurance policy is the simplest and most affordable type of coverage you can buy. It provides a death benefit for a specific, predetermined period, such as 10, 20, or 30 years.

Unlike temporary term policies, whole life insurance is designed to provide coverage for your entire lifetime. Because insurance companies guarantee a payout eventually, premiums are significantly higher than those for term policies.

If you are looking for permanent coverage with greater flexibility and growth potential, an indexed universal life (IUL) policy is a powerful option.

Also known as burial insurance, final expense insurance is a small whole life policy specifically designed for older adults.

Which type of life insurance is best for me? The best policy for you depends entirely on your financial goals, your current budget, and the specific life events you are trying to protect against.

When you sit down to compare life insurance options, you have to weigh the upfront cost against the long-range benefits. If your primary goal is maximizing your death benefit while keeping your monthly costs as low as possible, a term policy is the clear winner. However, if your goal is estate planning, leaving a permanent legacy, or building tax-advantaged wealth, permanent policies like whole life or universal life are superior tools.

To compare life insurance effectively, consider these key comparisons:

You should always compare life insurance products side by side with a licensed advisor to ensure you make the most informed decision possible for your household.

How much life insurance do I really need? Financial experts universally recommend purchasing a life insurance policy with a death benefit equal to 10 to 15 times your annual gross income.

While that rule of thumb is an excellent starting point, conducting a detailed needs analysis will give you a much more precise figure. We recommend using the DIME formula:

Once you add those four pillars together, subtract any existing liquid savings or group coverage you already have through your employer. The resulting number is your exact coverage gap.

When determining your ideal coverage amount, it is absolutely critical to account for inflation. A half-million-dollar death benefit might seem massive today, but in thirty years, its purchasing power will be significantly diminished. To protect your family against inflation, consider purchasing an increasing term policy whose payout increases annually. Alternatively, you can attach a specific cost-of-living rider to your permanent life insurance policy.

After deciding on the type and amount of coverage, you must go through the underwriting process. This is how the insurance company evaluates your overall risk profile to determine your premium rate.

Historically, securing a life insurance policy required a lengthy medical exam. A paramedical professional would visit your home to measure your height and weight, check your blood pressure, and collect blood and urine samples.

Today, the industry has modernized rapidly. Many top-tier carriers now offer accelerated algorithmic underwriting. This process uses real-time information to provide instant approvals to qualified applicants, bypassing the medical exam entirely.

However, you must be aware that algorithms use non-medical lifestyle data points, often referred to as a TRL score. This means that factors completely unrelated to your physical health can negatively impact your rates. For example, a recent drop in your credit score from buying a house, a past bankruptcy, or a reckless driving charge can push you out of the best rate classes. If your lifestyle data flags the algorithm, you will likely be routed back to traditional underwriting.

Getting affordable life insurance requires a bit of strategy and an understanding of consumer rights. Here are essential consumer tips to keep in mind during the buying process:

To make your life insurance policy as robust as possible, you can add optional provisions known as riders. These add-ons let you tailor the contract to your exact lifestyle and future needs.

Life insurance is not simply a tool for covering final expenses. When used strategically, it becomes a strong asset for wealth management and estate planning.

Life insurance plays a key role in diverse communities. Statistics show that Black Americans are highly likely to depend on life insurance to meet immediate expenses, yet they historically hold significantly smaller policies than white families with identical financial profiles.

Changing the narrative is essential. By shifting away from small burial policies and utilizing permanent whole life insurance to accumulate tax-advantaged cash value, minority families can strategically build and transfer generational wealth. A substantial, tax-free death benefit ensures the next generation begins their financial journey on a solid foundation.

Business owners face unique risks that can be mitigated through specialized life insurance strategies.

What happens if you reach your golden years, your mortgage is paid off, your children are financially independent, and you simply can no longer afford the premiums on your permanent life insurance policy? You do not have to let it lapse or surrender it for pennies on the dollar.

You have the right to pursue a life settlement. This involves selling your policy to a third-party investor for an immediate cash payment. The payment will be greater than your policy surrender value but less than the total death benefit. The investor becomes the new owner, assumes the premium payments, and eventually collects the payout. This strategy can provide a significant cash injection to help fund your retirement or cover long-term healthcare costs.

Savvy buyers rarely rely on a single policy. Instead, they use a strategy called laddering. You might purchase a 30-year term life insurance policy to protect your spouse, a 20-year term policy to cover your mortgage, and a 10-year term policy to cover your children’s education. As each term expires, your overall coverage amount and your premium costs decrease naturally as your debts shrink.

If you already own a permanent policy but find a newer product with better cash value growth potential, you can utilize a 1035 Exchange. This specific IRS tax code provision allows you to transfer the accumulated funds from your old policy directly into a new one without triggering a taxable event.

The insurance industry is highly regulated to protect consumers. Knowing these safety nets are in place will give you total peace of mind.

It is incredibly common for families to realize a deceased loved one had coverage, but they have no idea where the paperwork is located. If a policy is forgotten for years, the payout may eventually be transferred to a state unclaimed property office.

To prevent this frustrating scenario, beneficiaries can utilize free state-run Lost Policy Finder tools. These official government databases help families locate unclaimed death benefits without charging any recovery fees. It is always best practice to ensure your life insurance beneficiary knows exactly where your documents are stored and who your agent is.

A usual concern among beginners is whether their death benefit is truly safe if the insurance carrier goes bankrupt. In the United States, your policy is heavily protected by state guarantee associations.

If a licensed insurance company becomes insolvent, the state Guaranty Fund steps in to ensure that valid claims are paid. In most states, the fund provides up to $500,000 in safety net protection for death benefits. This ensures your family will not be left empty-handed, even in the worst-case scenario of corporate bankruptcy.

While educating consumers is our primary goal, delivering these sophisticated solutions requires advanced tools. The modern client demands precise, data-driven advice. This is exactly where the Life Policy Express platform transforms an insurance agent’s practice, allowing them to serve as holistic financial fiduciaries rather than just policy salespeople.

As instant-approval algorithms become the industry standard, agents risk seeing their clients penalized for non-medical data points. Life Policy Express provides advanced pre-underwriting triage tools. Agents can securely screen a client’s lifestyle factors (such as recent credit dips or driving infractions) before submitting a formal application. This enables the agent to pivot high-risk clients toward traditional medical underwriting, making sure they secure the most favorable rate class possible.

Standard consumer calculators rarely account for the thirty-year erosion of purchasing power. Life Policy Express equips agents with dynamic, inflation-adjusted quoting software. These visual calculators vividly demonstrate how inflation will impact a death benefit over time. By proving the coverage gap, agents can smoothly recommend advanced laddering strategies or specific cost-of-living riders.

When senior clients can no longer afford their permanent premiums, traditional agents often watch the policy lapse. Life Policy Express empowers agents with evaluation models for life settlements. By helping seniors safely sell their unneeded policies to third parties for immediate cash payouts, agents cement their status as lifelong, trusted advisors who actively protect their clients’ assets.

To ensure a family never has to manage a state Lost Policy Finder, Life Policy Express features digital legacy-organizing tools. Agents can construct secure digital portfolios for their clients that consolidate carrier details, policy numbers, and direct contact information. When the unthinkable happens, beneficiaries have instant access to exactly what they need to file a claim seamlessly.

We hope this life insurance guide has demystified the process for you. Remember, the core purpose of a life insurance policy is to provide your family with unshakeable financial security. By understanding your options, conducting a thorough needs analysis, and handling the underwriting process strategically, you can secure the perfect plan for your unique situation.

Do not let the fear of complex jargon delay your financial planning. As you wrap up reading this complete guide to buying life insurance online, take the opportunity to review your own financial standing. We designed this content to ensure that having life insurance explained for beginners leads directly to confident, knowledgeable action.

Are you prepared to take the next step? It is time to explore options customized specifically to your needs. Start by gathering customized life insurance quotes today. Comparing different life insurance quotes will ensure you get the best value for your hard-earned money. Bookmark this life insurance guide for your annual financial reviews, and secure your life insurance quotes to begin building your legacy.