Discover transparent final expense life insurance options for seniors. Compare no medical exam life insurance plans with a local policy express advisor today.

It is not easy to think about the costs that come at the end of life, but final expense life insurance can help make things simpler for families and seniors. In this guide, you can find explanations on how these policies work, who they are meant for, and what you should know before making a decision. My goal is to help you feel more at ease as you talk about this important topic.

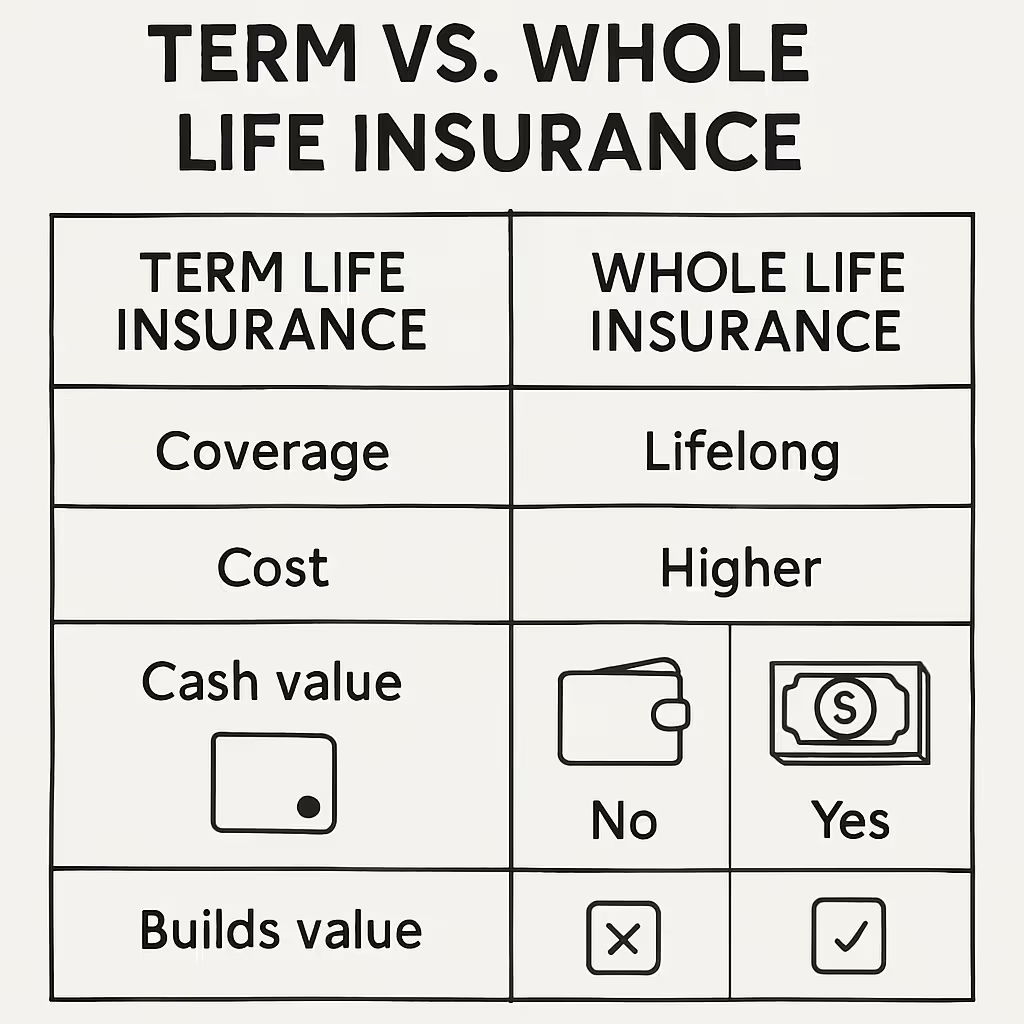

Final expense life insurance is a type of whole life policy that helps cover expenses such as funerals, medical bills, and other costs that arise at the end of life. You do not have to undergo a full medical exam to be covered, and your payments will not increase as you get older. Over time, your policy can also build up a little cash value.

This structure helps keep the policy in force for the insured's entire life, as long as premiums are paid. Unlike term products that end after a set number of years, final expense life insurance offers long-term certainty for seniors. The cash value grows over time at a fixed rate, providing a dependable financial asset.

The main feature of these policies is an easier application process, often using no-medical-exam underwriting. This approach eliminates the need for blood draws, physical checkups, or fluid testing, making it a useful option for older adults who might otherwise be excluded because of chronic health conditions. Instead of medical testing, underwriting decisions rely on brief health questions.

How much you pay for final expense insurance depends on your age, whether you are male or female, how much coverage you want, and your answers to a few health questions. Since these plans are easier to qualify for, the monthly cost is usually a bit higher than other types of life insurance that require a full medical exam.

To avoid paying for more coverage than needed, consumers should compare how different policy types affect overall affordability. Older adults looking for life insurance for seniors usually encounter three main plan types, each with a different cost level and benefit structure.

These plans are usually the most affordable for seniors who have only minor health issues. You will answer a few questions about your health, like whether you have had a stroke or are being treated for cancer. If there are no major problems, you can get full coverage right away, starting from your first payment.

If you have had some recent health problems, like diabetes with a few complications or past heart treatments, a graded plan might be a good fit. These plans cost more than standard ones, and the payout is on a schedule. If you pass away within the first two years, your family receives a portion of the benefit, which increases each year until it reaches the full amount.

This option provides a reliable safety net for applicants facing serious, chronic health problems or cognitive impairments. These plans eliminate health questions and medical exams, so coverage cannot be denied based on medical history. Because the carrier accepts more risk, premiums are in the highest cost tier for cheap insurance life lookups, and the plan includes a required 24-month benefit waiting period.

Final expense life insurance can be a good choice for seniors who do not have extra savings to cover funeral costs and want to make sure their family is not left with a sudden bill. It gives your loved ones tax-free money right when they need it most.

For many families, it is about considering the monthly cost against the peace of mind that comes with knowing final expenses are covered. Without this kind of help, loved ones can be left with big bills at a very hard time.

Permanent final expense insurance stands out when you compare it to other ways of saving. If you just use a regular savings account, your family might have to wait months to access the funds due to legal delays.

If your family has to use credit cards or loans, they could end up with high-interest debt. With a whole life policy, the money goes straight to your loved ones, tax-free, and without any legal holdups.

A frequent point of confusion for seniors involves the operational differences between independent final expense protection and pre-need agreements managed directly by individual funeral homes. Although both approaches address end-of-life costs, their legal structures and financial flexibilities are entirely distinct.

Pre-need agreements typically bind insurance funding directly to a single, specific mortuary provider. If the insured individual moves to another state, or if the chosen funeral home goes out of business, relocating or recovering those funds can involve major legal hurdles and contract termination fees.

In contrast, an independent permanent whole life contract pays out cash directly to chosen beneficiaries. According to MoneyGeek, final expense insurance provides a death benefit that your beneficiary can use for a variety of end-of-life expenses, such as funeral and burial costs, medical bills, and small debts, offering flexibility in how the funds are spent without limiting use to a particular funeral home. Funeral home arrangements, on the other hand, typically address specific, on-site charges like caskets, burial plots, and cremation fees. However, when an individual passes, families commonly confront secondary expenses that fall outside the scope of a standard mortuary agreement.

These can include outstanding regional medical costs, unresolved credit card accounts, or travel expenses for out-of-town relatives. The cash payout from a final expense policy can be used flexibly to meet any of these important financial needs.

Before completing a permanent policy application, buyers should carefully evaluate other major contracts with a trusted advisor. This review ensures that the selected coverage is consistent with long-term household financial planning goals.

Every life insurance contract includes a standard 24-month contestability period that begins on the initial effective date. During this time, the carrier has the statutory right to verify the accuracy of the health declarations on the application if a claim occurs.

Working with a dedicated professional at a trusted service like Life Policy Express ensures your health history is accurately documented from day one, protecting your policy against future documentation errors.

As policyholders grow older, the underlying actuarial risk increases. In a permanent whole life design, the premium remains flat because the contract overcharges for risk during the early years to balance out the higher risk in later years.

This mechanism allows the policy to accumulate an internal cash value. Understanding how this cash value accumulates over time helps policyholders evaluate features such as policy loans or extended-term conversions if their financial situation changes.

Getting final expense insurance is really about helping your family when they need it most. By planning ahead, you make sure your loved ones are not left to handle high costs on their own during a difficult time.

Life Policy Express helps families make these important choices with clear information and respect. By connecting you with local advisors and avoiding call center hassles, they make it easier for seniors to protect their legacy with confidence and personal care.