Skip the medical exam and get life insurance coverage fast. Learn about the 4 types of no-exam policies, the trade-offs, and if it's the right choice for you.

When most people hear 'life insurance,' they picture doctor appointments, blood tests, and weeks of paperwork. That worry keeps a lot of families from getting the coverage they need. The good news is that no-exam life insurance lets you get covered in just days, sometimes even hours, and you do not have to deal with needles.

Consider a working parent in their early 40s who needs coverage quickly before an international business trip. With traditional underwriting, they might wait 30 to 60 days for approval. With a no-medical-exam life insurance policy, they could walk away with coverage the same afternoon. That speed and simplicity are genuinely valuable.

Skipping the exam does come with trade-offs. You will usually pay higher premiums, and there may be limits on how much coverage you can get. Before you choose, make sure you know what you are giving up and if it makes sense for you. This guide will help you sort it out.

One thing to clear up right away: 'no exam life insurance' does not mean you get approved automatically or skip all questions. Insurers still check your risk carefully. They just use software instead of a stethoscope.

Modern carriers use state-of-the-art algorithms and third-party data sources to build a risk profile of each applicant in minutes rather than weeks. These databases may include:

For most simple cases, this risk check is just as accurate as a physical exam. There is a real trade-off with data privacy, but traditional life insurance uses these records too. Insurers have always checked third-party data.

With data-centric underwriting, being honest is not just the right thing to do. It is also practical. Insurers check your answers against prescription records and medical databases. If something does not match, they notice right away.

If the insurer finds out about a pre-existing condition after you file a claim, your family could get less money or even have the claim denied. That defeats the whole point of having life insurance. Always answer every question honestly and fully.

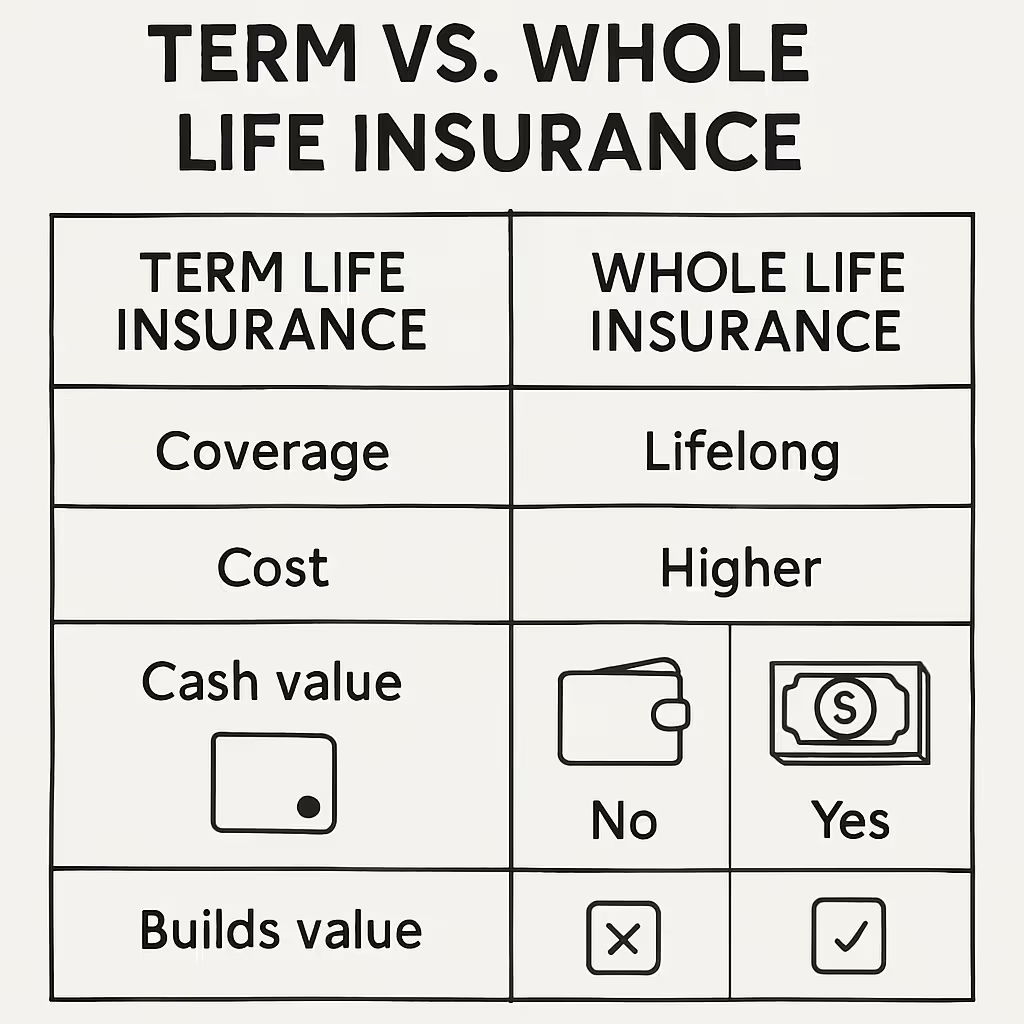

Not all no-exam life insurance policies work the same way. There are four distinct product types, each having its own trade-offs.

Accelerated underwriting is for healthy people, usually under 60, who want to skip the medical exam but still get good rates. If your records look good, you can get coverage up to $1 million or more, often at the same price as traditional policies.

It is like a traditional policy, just faster. You still answer health questions and the insurer checks your records, but there is no medical exam unless something unusual comes up. For healthy people, this is usually the best choice.

Simplified issue life insurance asks you to fill out a health questionnaire, but you do not need a physical exam. You can usually get approved in a few days. The catch is that coverage is usually limited to $250,000 to $500,000, and you will pay more than you would for a traditional policy.

For example, a healthy 45-year-old could pay 20% to 40% more each month for a simplified issue policy compared to a traditional one. Over 20 years, that extra cost really adds up.

Guaranteed issue life insurance does not ask any health questions and accepts everyone. It is meant for people with serious health problems who cannot get other types of coverage. The coverage amounts are small, usually $5,000 to $25,000, and it is the most expensive option per dollar of coverage.

Many employers offer basic group life insurance without a medical exam. You get coverage automatically, usually up to one or two times your yearly salary, and your employer often pays part of the cost.

One thing many people miss is that group life insurance is connected to your job. If you leave or get laid off, you usually lose the coverage. Some employers let you convert it to an individual policy without extra health checks. It is a good idea to check your benefits now, before you need them.

Life insurance without a medical exam makes the most sense for:

If you are healthy and have big financial responsibilities, a traditional policy with a medical exam will usually give you more coverage for less money each month. For example, a healthy 35-year-old couple with a $500,000 mortgage and two kids could save tens of thousands of dollars over 20 years by taking the exam. That savings could go toward college or retirement.

The bottom line: if you are healthy, the exam is worth it. If speed, health conditions, or convenience are overriding factors, no-exam life insurance is a legitimate and valuable option.

If you get turned down by an accelerated underwriting process, it does not mean you cannot get life insurance. Sometimes the system just flags something unusual and sends your case for more review. You might be asked to fill out more forms, provide doctor records, or take a regular medical exam.

The important thing is not to give up. Work with an agent who can check with different companies, since their rules are not all the same. A medication that is a problem for one insurer might not matter to another.

Most people are surprised to learn that you usually do not have to take a full medical exam, even for traditional life insurance. Some big companies only require exams for less than 10% of applicants. Exams usually happen only if you want a lot of coverage, have a high BMI, or are over a certain age.

If you do need an exam, it is usually much easier than people think.

For buyers who know what to look for, no-exam life insurance is pretty simple. For agents, it is more complicated. They have to match clients to the right process, keep up with different company rules, and respond quickly if a client is marked. Life Policy Express is designed to help with all of that.

When a client is weighing the higher cost of a simplified issue life insurance policy against the commitment of a traditional exam, the conversation should be data-driven. Life Policy Express equips agents with instant quoting tools that pull side-by-side comparisons across multiple carriers in real time, allowing agents to show clients the exact dollar-for-dollar trade-off. That transparency creates trust and closes more cases.

Accelerated underwriting depends a lot on each company's rules. One insurer might deny someone because of a prescription, BMI, or driving record, while another might approve them. Life Policy Express helps agents check these details ahead of time, so clients are less likely to get rejected.

When a client is declined for accelerated underwriting, momentum matters. Losing the sale because you do not have an immediate alternative costs both the agent and the client. Life Policy Express gives agents the infrastructure to pivot instantly, moving a declined accelerated underwriting applicant into a simplified issue or guaranteed issue life insurance application without losing the client's trust or the case.

That is the kind of platform capability that separates agents who close consistently from those who lose business to process friction.

Ready to offer your clients a faster path to coverage? Compare no-exam life insurance quotes in minutes through Life Policy Express, or join our agent network to access instant quoting, carrier matching, and a built-in Plan B for every client. [Get a no-exam quote] | [Join the Agent Network]