Ready to compare life insurance quotes online? Use the DIME formula to find your coverage, understand underwriting, and select the best policy and riders.

Many families face a turning point with money when a loved one passes away. Suddenly, the bills keep coming, but the financial safety net they expected is missing. The mortgage is still due. Groceries and tuition do not wait. Life insurance protects families from this kind of shock. The key to getting the right life insurance policy at the right price is knowing how to compare life insurance quotes online with an analytical eye, not just by selecting the lowest number on a screen.

Most people spend more time researching a smartphone than they do with a life insurance quote comparison. That gap is understandable: the topic is unfamiliar, the jargon is dense, and no one enjoys thinking about mortality. But the stakes are high enough to change that habit. A policy that looks affordable on the surface can carry hidden limitations that make it far less valuable than a slightly higher-priced alternative. Knowing how to read and compare life insurance quotes properly is one of the most important financial skills you can develop.

This guide goes beyond the basics. Rather than simply explaining what life insurance is, it focuses on the how: how underwriting actually works, how to build a genuine apples-to-apples comparison, how to assess a carrier's financial strength, how to decode riders and fine print, and how to make smart choices concerning data privacy when getting quotes online. If you are ready to get started comparing life insurance quotes like a professional, this playbook is your starting point.

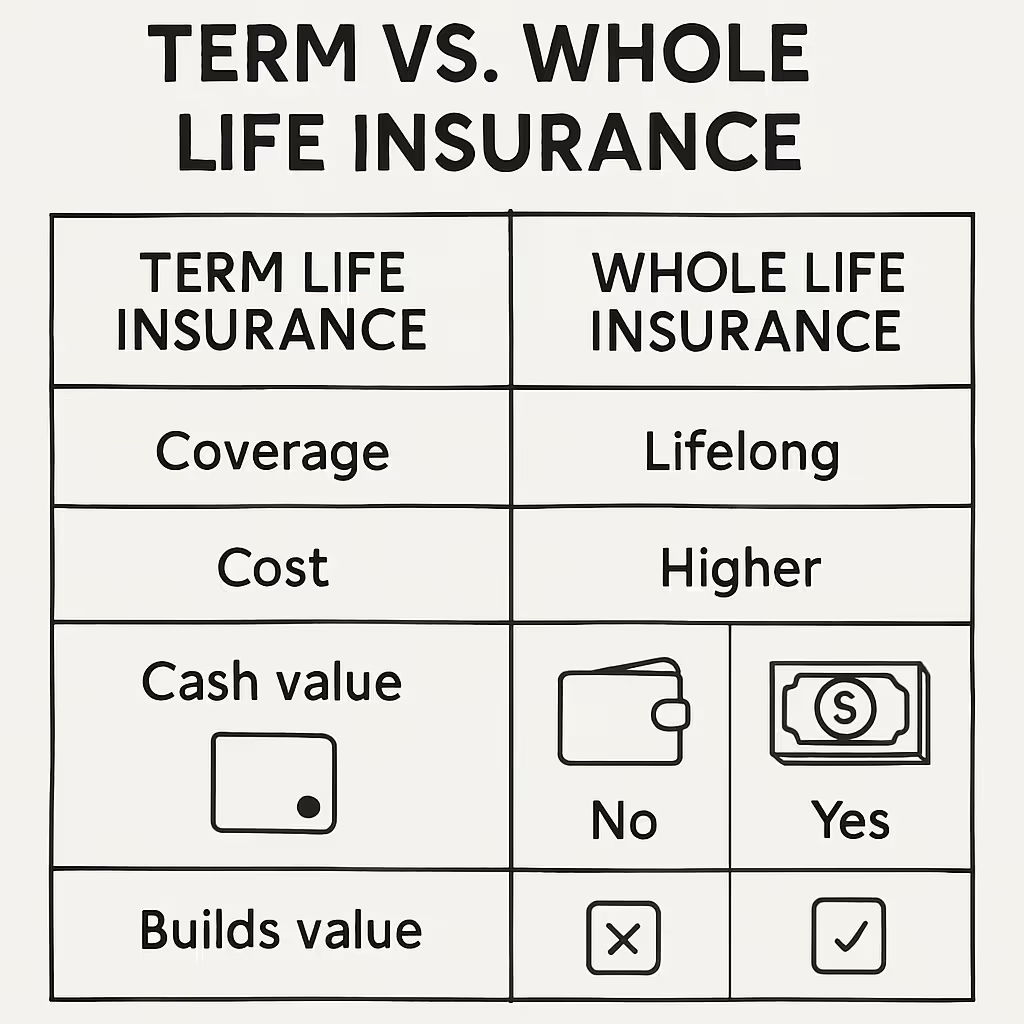

Before you start comparing life insurance quotes online, you need to understand the two main types of policies. Comparing them without knowing the difference is like comparing the price of a studio apartment to a four-bedroom house and expecting them to match.

Term life is often described as pure protection. You pay a level premium for a defined period, commonly 10, 20, or 30 years, and if you die during that window, your beneficiaries receive the death benefit tax-free. If you outlive the term, the coverage ends, and no cash value accumulates.

A financial planner would say term life is designed for a specific need. For example, a 35-year-old with a 30-year mortgage, two young kids, and a partner who depends on their income faces a clear financial risk for a set period of time. A 30-year term policy covers that time at a much lower cost than permanent insurance.

When term life is the most practical choice:

Permanent policies, including whole life and universal life, provide coverage for your entire lifetime as long as premiums are paid. They also include a cash value component that grows on a tax-deferred basis and can be accessed through loans or withdrawals during your lifetime. [2]

Permanent policies cost much more than term policies for the same coverage. The higher price pays for lifelong protection and the cash value feature. Some people find this worth it. Others get better results by choosing term life and investing the difference.

One of the most common mistakes buyers make when shopping for affordable life insurance is working backward from a monthly premium they feel comfortable paying, rather than working forward from a death benefit their family actually needs. The result is chronic underinsurance, a gap that becomes painfully apparent precisely when the policy is needed most.

A widely used starting point is to target a death benefit equal to 10 to 20 times your annual gross income. A household earning $80,000 per year would therefore consider coverage between $800,000 and $1.6 million. The range exists because individual circumstances vary considerably. A 40-year-old with no debt, a fully funded emergency account, and a working spouse with a closer to $800,000. A 40-year-old with a substantial mortgage, three children, and a stay-at-home spouse needs coverage closer to the upper end of that range.

For buyers who want to move beyond rules of thumb, the DIME formula provides a structured framework:

Once you have calculated that total, subtract any existing financial resources: savings, existing life insurance policies, a spouse's income stream, or other liquid assets. The result is your coverage amount target, the number that should anchor your life insurance quote comparison, not the other way around.

Every life insurance quote you receive online is an estimate. It reflects the rate a carrier would offer to an applicant in average or standard health. Your actual, locked-in premium, called the underwriting decision, is determined after the insurer evaluates your individual risk profile. Understanding what goes into that assessment helps you anticipate where your rate might land and identify steps you can take before you apply to improve it.

Insurers evaluate a structured set of variables when pricing a policy:

Carriers group applicants into risk classes that determine the final life insurance premium. While naming conventions vary by insurer, the general hierarchy looks like this:

This is why shopping for affordable life insurance is not simply about getting quotes from different companies. You also need to find carriers whose rules work best for your health situation. For example, if you have well-managed Type 2 diabetes, some companies will offer you better rates than others, even if their standard rates are not the lowest.

With your coverage target established and a working understanding of underwriting, you are ready to build a genuine life insurance quote comparison. The mechanics are straightforward. The discipline required to do it correctly is where most buyers fall short.

The lowest quote you see is only the lowest in that group. It does not always mean the best value, reliability, or a good fit for your needs. Keep these three rules in mind for a fair comparison:

Two policies with identical premiums and death benefits can differ significantly in value based on what happens under specific circumstances. Riders are the mechanism through which that differentiation occurs. Policy riders are optional add-ons, or sometimes standard inclusions, that expand the conditions under which the policy pays benefits. Key riders worth evaluating include:

Not every rider is right for everyone. An accelerated death benefit is usually a good idea. A return-of-premium rider depends on your finances and what you could earn elsewhere. A licensed advisor can help you see what works best for you.

Applying for life insurance is much different now than it used to be. You can choose between traditional policies with a medical exam and newer options that skip it. Knowing the pros and cons helps you pick what fits your needs.

A fully underwritten policy requires a medical exam, typically conducted by a paramedical professional at no cost to you, and a complete review of your medical records. The examination generally includes height, weight, blood pressure measurements, and a blood and urine panel. Some carriers also request an EKG for applicants above a certain age or coverage threshold.

Full underwriting usually means lower premiums if you are healthy and take the medical exam. The insurer feels more confident about your risk. The downside is that it takes longer, often four to eight weeks from start to finish.

The no-exam life insurance category has expanded considerably, and it is worth distinguishing between two distinct types:

If you are healthy and under 50, accelerated underwriting usually gives you fast approval and good rates. If your health is more complex, find companies with good underwriting guidelines for your condition and consider full underwriting.

Online quote sites differ in their approach to privacy. Some connect you with a real advisor. Others just collect your information to sell it to many agents. This difference matters more than most people think.

When you enter your name, phone number, date of birth, and health information into an online quote form, you are sharing sensitive data. Before submitting that form, confirm that the platform clearly discloses how your information is used, whether it will be shared with third parties, and how you can opt out of communications. Life insurance lead aggregators that sell your data to dozens of agents simultaneously are a well-documented source of aggressive, unwanted outreach. Working with a platform that matches you to a single licensed advisor protects both your privacy and your time.

Lowering your life insurance premiums is not complicated. The best ways are simple and work best if you plan ahead.

Age is the single most reliable predictor of life insurance cost. Every year you delay adds to your risk profile in the actuarial tables carriers use to set rates. A 30-year-old purchasing a 30-year $1 million term policy will qualify for a substantially lower premium than a 40-year-old purchasing the same policy, even if both are in identical health. The cumulative difference in premiums paid over the life of the policy can be significant.

Getting life insurance while you are young and healthy is one of the easiest ways to save money. Prices go up as you age or if your health changes. Buying early means lower rates and longer coverage.

The medical exam for life insurance is not pass-or-fail. It puts you in a risk group, which sets your premium. Making a few health-related changes before you apply can help you get a better rate.

Two payment-related strategies can reduce the total cost of your policy without changing the coverage itself:

The process of comparing life insurance quotes online has historically been fragmented for both agents and buyers. Agents working with multiple carriers have often managed separate quoting tools, carrier portals, and paper-intensive workflows that add hours to what should be a straightforward client conversation. Life Policy Express was built to address that inefficiency directly.

The Life Policy Express platform enables agents to generate side-by-side life insurance quote comparisons from multiple top-rated carriers in a single session. Rather than logging into individual carrier portals and manually reconciling outputs, agents can present a clean, comprehensive comparison to a client in real time. This kind of transparency is not just about operational efficiency. It builds client confidence at the most important moment in the sales conversation.

Old quoting methods with lots of paperwork slow things down and turn off buyers, especially younger ones. A smooth digital process keeps people engaged and makes it easier to go from quote to application. Agents who can do this in one meeting close more sales.

Automated quoting and easy data collection save agents from time-consuming paperwork. With these steps handled by the platform, agents can focus on what matters: helping clients figure out their coverage needs, explaining underwriting, and recommending the right policy and riders for each family.

This is what Life Policy Express is all about. The technology handles the busywork so advisors can focus on building trust and giving real advice that leads to lasting client relationships.

The ability to compare life insurance quotes online has genuinely democratized access to coverage. A buyer today can receive quotes from dozens of top-rated carriers without leaving home, without scheduling multiple appointments, and without sitting through high-pressure sales presentations. That is a significant improvement over the process that existed a generation ago.

Technology only helps if you have the right plan. If you get quotes without knowing how much coverage you need, how underwriting works, or how to check riders and company strength, you are just guessing. The numbers will not make sense, and you might default to the cheapest option, which is often not the best choice.

The steps in this guide—figuring out your coverage, understanding underwriting, making fair comparisons, and working with a trusted advisor—lead to better results. You get a policy that really protects you, a premium that suits your risk, and decisions made with confidence.

Now that you know the process, it is time to put it into action.

Start by calculating your actual coverage needs using a method such as the DIME formula. Then request quotes from multiple carriers with identical term lengths and death benefit amounts. Evaluate each quote alongside the carrier's financial strength rating and the policy's rider options before making a decision. The lowest premium is only the best outcome if everything else in the comparison is equivalent.

It is safe when you use a reputable licensed platform that clearly discloses how your information is used and does not sell your data to third-party lead buyers. Be cautious of aggregator sites that require you to accept contact from multiple agents as a condition of receiving a quote. A platform that matches you with a single licensed advisor offers far better data privacy.

The cheapest policy relative to the coverage it provides is typically a term life policy purchased by a young, healthy, non-smoking applicant through full underwriting. Premiums increase with age, tobacco use, weight, and health history. No-exam life insurance is convenient but usually carries higher premiums than fully underwritten alternatives for healthy applicants.

Look for identical coverage amounts and term lengths across all quotes you are comparing. Verify the carrier's financial strength rating through A.M. Best or Standard and Poor's. Evaluate key riders, particularly the accelerated death benefit, waiver of premium, and conversion privilege. Review the policy's exclusions and any graded benefit provisions carefully.

Three to five quotes from highly rated carriers are typically sufficient to establish a competitive baseline. More quotes are useful if you have a complex health profile, because underwriting guidelines vary significantly between carriers, and the carrier whose guidelines are most favorable for your specific situation can offer a substantially better rate.